v## Bonds

DEFINITION

(risk-free rate, usually government bond yield) is the required rate of return.

You discount by it to find the value of a dollar in the future.

Money loses value over a time. A dollar today is worth more than a dollar tomorrow (due to loss of investing potential).

Bond Price (Present Value)

A bond’s price is the present value of all future cash flows discounted at the required rate of return (yield to maturity):

where is the periodic coupon payment, is the face value, and is maturity.

The price adjusts so that the bond’s effective return equals . The coupon rate determines if the bond is “worth it” and adjusts price (below or above par). If it’s not high enough, you lose money in comparison to “just invest in something that gets you “.

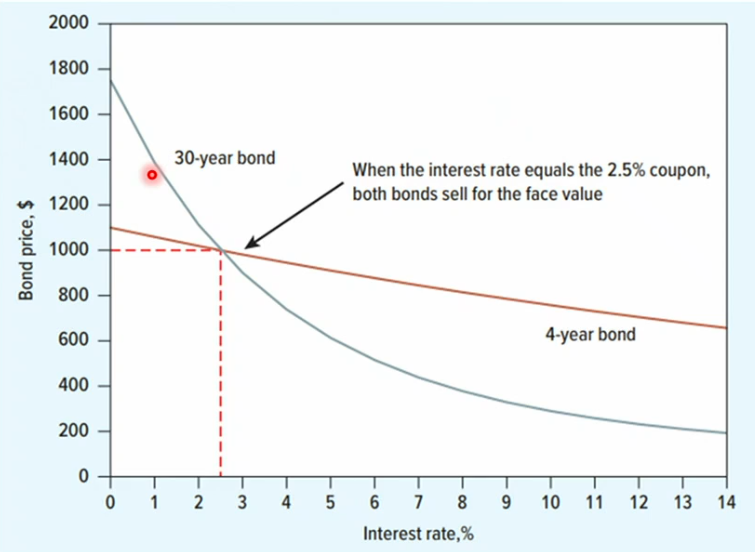

Bond prices and interest rates move inversely: if , then , and vice versa. Longer maturities amplify this sensitivity, since the large repayment is discounted over more periods.

When the maturity of a bond is longer (i.e. longer until it pays out the par), it costs less, since the risk of changing is higher.

Example Calculation:

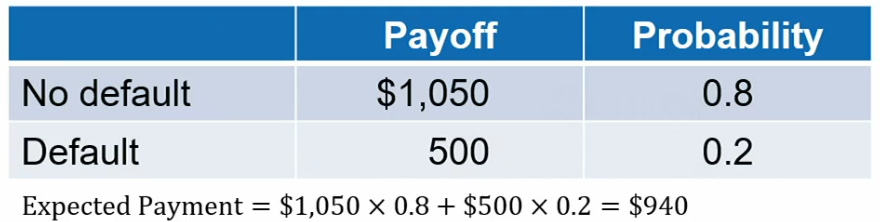

The is , thus it would sell for \frac{par + cpn}{market value} - 1 = \frac{1050}{895} - 1 = 17.3%\frac{50}{1000} = 5%$. But since the market compensates you for taking the risk you get a premium.

But in the end, you only EV 950/895 = 1.05%5%$. In reality, the market would demand more than 5% for risk compensation.

Credit spread = bond yield - treasury yield. Note, very important to choose same maturity! So for a bond with 2.36% yield and treasury of 0.676%, we get a spread of 1.684%. This will be higher for lower rated bonds - risk premium!

Yield Spread across eco-cycles

Yield-spread changes with economic cycles

Bond Value Calc (Merton Model)

THEOREM

Merton model = limited liability of shareholders gives equity holders an option-like payoff on the firm’s assets.

Bond value = bond value assuming no chance to default - (value of put option on assets)

Option to Default - PUT Option

Put Option

A put option = the right to sell an asset at a fixed price (the strike), regardless of actual value.

- If asset value < strike → exercise (profitable)

- If asset value > strike → ignore

Default Put

Put payoff =

where F = face value of debt, is value at maturity.

Under the Merton Model, the default put has:

- strike = face value of debt

- underlying = asset value

- maturity = debt maturity T

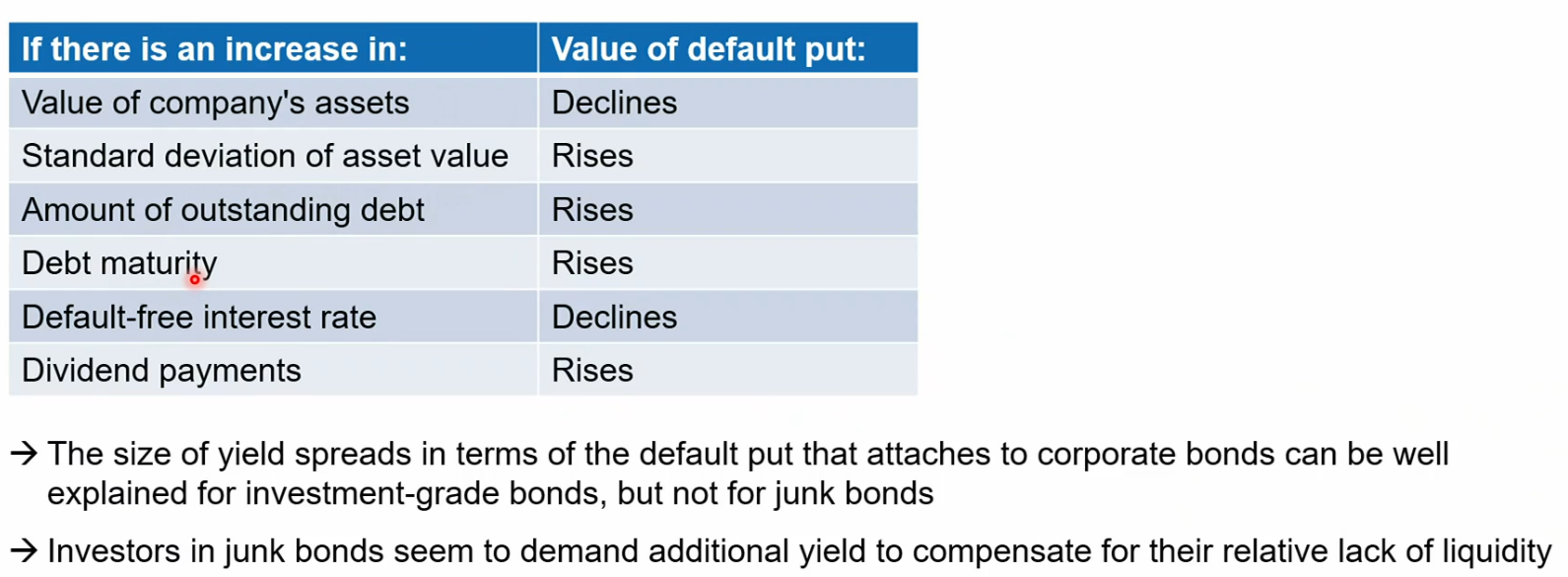

If the assets increase, the put value declines, as the underlying increases (prob. of default falls, as more cash)

If risk-free rate increases, the strike is discounted more. As PV(F) decreases, (F - V) decreases and the put loses value.

Merton Model bond value

A Corporate bond = risk-free bond − default put

Note: higher interest rate decreases default put value → narrows yield spread as less risky.

Shareholders hold a put on firm assets with strike = face value of debt (e.g. $50).

- Assets < $50 at maturity → default, hand over assets, walk away (limited liability)

- Assets > $50 → repay bond, keep the surplus

Bond = , Firm assets = . Basically the shareholders have the option to run away:

- they got from the bondholders

- Hand over all assets → owe them only .

- So profit (from what the bondholders originally paid)

Why the put is more valuable when the firm is broke

The put is in the money when assets < strike. The deeper the firm is underwater, the more valuable the right to walk away — bondholders absorb all extra downside.

Implication: Riskier/more volatile firms → more valuable default put → bonds trade at a bigger discount → higher yields demanded by bondholders.

Overview:

If dividends are paid out, the default put value rises → shareholders took out money from the assets of the company and paid out. Thus the assets are worth less → put is more in the money.

junk bond investors want higher yield → liquidity risk AND distress risk → during economic downturns, defaults will cluster.

Bond Ratings

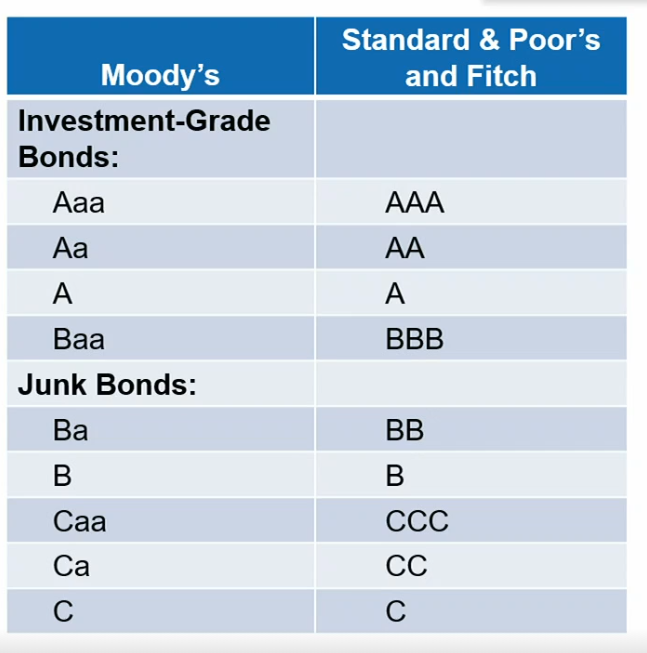

Credit Rating Agencies like Moody’s, Standard & Poor’s.

The correlation between different firm’s ratings is very high - in comparison to ESG ratings.

Baa is the lowest that is still investment-grade

Ba is junk

Bond terminology

Indenture The name of the contract between the bond issuers and bondholders → it specifies all legal details.

Registered Bond When people say bond, they usually mean ‘registered bond’ today. Name and details of the owner are registered, coupons are paid out automatically.

Covenant

- terms associated with the bond → written into contract

- most commonly merger restrictions

Accrued interest

- coupon * days since last coupon / days in coupon period

- an extra on what the bond is worth based on how long it has been held (i.e. risk) = portion of the coupon payment that has “built up” since last coupon paid but hasn’t been paid out yet

- Dirty price = clean price + accrued interest (clean quoted to make comparable, but you still have to pay the dirty price)

Callable bonds

- The issuer (company) retains the right to recall it back early - i.e. pay out the par + coupon.

- If interest rates fall, the issuer can refinance cheaply. Call the old bond and issue a new one at a lower rate.

- Because the call benefits the issuer, investors demand a premium.

Bearer Bonds

- Bondholder must send in coupons to claim interest and send a certificate to get final payment of the principal.

Note: difference to registered bond = no record of the owner’s name and details.

Mortgage Bond

- corporation issues bond, backed by their own assets (factory, land, building)

Asset-Backed Security

- sell a bond on a bundle of loans the issuer made.

- It’s a special purpose vehicle SPV

- SPV issues securities to investors - they get the principal + interest from the underlying loan pool

- Lets lenders offload risk and free up capital

- Mortgage-Backed Security (or MB pass through certificates - as the interest is passed through) is an ABS but backed by mortgages.

Not the same as a Mortgage Bond

Foreign Bond

- sold to local investors in another country’s bond market

- ex: swiss company issues a bond in the US, denominated in USD (yankee-bond)

- samurai bond: “bond sold by a foreign firm in japan”

- bulldog bond: “bond sold by a foreign firm in the UK”

Eurobonds

- issued outside of the country of the currency they’re denominated in

- ex: us company issues USD-denominated bond in Europe (eurobond)

- less regulated and cheaper to issue (less disclosure requirements)

Medium-Term-Note debt-security that matures in a relatively intermediate timeframe (2-10 years).

- can be offered on a rolling/ongoing basis through a dealer, flexible terms

- Sold through dealers (usually large amount registered with SEC and then issued rolling)

- Sits somewhere between short-term commercial paper and long-term bonds

A fixed rate MTN eliminates interest rate risk, since you can borrow at the same interest rate over the full time.

Debenture long-term Bond issued by gov. or company

- it’s unsecured → backed only by issuers general creditworthiness

Equipment trust certificates

- railroad companies for ex

- bond secured by the actual equipment (trustee owns the railroad until paid back)

Collateral trust bond

- secured corporate bond backed by financial assets

- typically stocks, bonds or other securities

- these are pledged as collateral by issuers

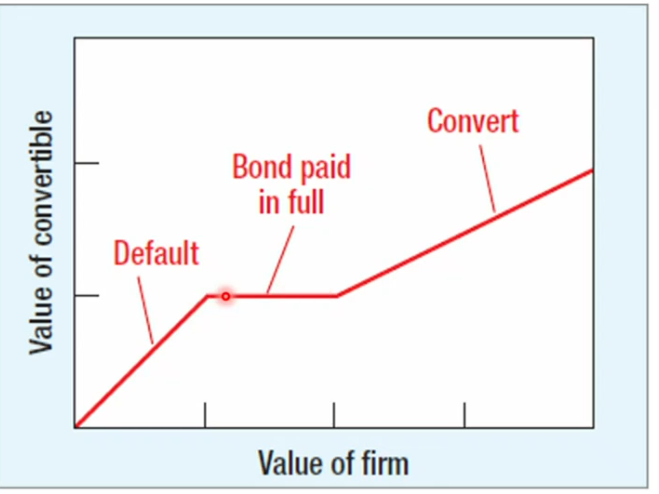

Convertible Bonds

- regular bond + a call option on the stock (pre-agreed conversion price)

- if stock price rises above conversion price (holder converts into shares and benefits) - bond ceases to exist

- better for the bond-holder (upside participation + bond floor = plain vanilla bond value without convertible option price = protection)

- company issues because lower coupon needed, never has to repay principal (good for cash - but ownership gets thinner)

For convertible:

Lower bound = higher of:

- straight bond value

- conversion value = conversion ratio * current stock price

it’s the higher of them because that’s what the bond-holder will choose

Upper bound = conversion ratio * current stock price

otherwise you could short shares and buy the convertible

- sometimes you can sell bond-warrant packages (compensation for the bondholders for risk)

- warrants are long-term call options (giving the investor the right to buy firm’s equity at pre-agreed price)

- can be separated

- the warrant means the company still has to repay the debt (not converted)

- company gets extra cash from the warrant-holder buying the shares (not converting) - but cheaper than at market rate

- the warrants are exercised for cash → company gets the cash from the holder to buy shares

- more dilution for company

Warrant

warrants are long-term call options (giving the investor the right to buy firm’s equity at pre-agreed price)

Sinking Fund

A fund established to retire debt before maturity. You pay a certain amount of the debt back into a special account (held by trustee). This guarantees that in case of default, at least part of the principal is returned.

Bond Covenants

To restrict the company from screwing you over by reshuffling, issuing new debt, etc… you agree to terms in the bond contract.

- Debt ratios — limits further borrowing (senior debt limits senior; junior limits both)

- Negative pledge — new secured bonds must give unsecured holders equal security

- Leasing — treated like secured borrowing

- Dividends — capped to protect repayment capacity

- Event risk — debt stays with the full merged entity after M&A

Goal: prevent wealth transfers from bondholders → shareholders.

Exotic Bonds

| Bond Type | Description |

|---|---|

| Asset-backed securities | Many small loans are packaged together and resold as a bond. |

| Catastrophe (CAT) bonds | Payments are reduced in the event of a specified natural disaster. |

| Contingent convertibles (CoCos) | Bonds that convert automatically into equity as the value of the company falls. |

| Equity-linked bonds | Payments are linked to the performance of a stock market index. |

| Longevity bonds | Bonds whose payments are reduced or eliminated if there is a fall in mortality rates. |

| Mortality bonds | Bonds whose payments are reduced or eliminated if there is a jump in mortality rates. |

| Pay-in-kind bonds (PIKs) | Issuer can choose to make interest payments either in cash or in more bonds with an equivalent face value. |

| Credit-linked bonds | Coupon rate changes as company’s credit rating changes. |

| Reverse floaters (yield-curve notes) | Floating-rate bonds that pay a higher rate of interest when other interest rates fall and a lower rate when other interest rates rise. Bet on falling interest rates by investors. |

| Step-up bonds | Bonds whose coupon payments increase over time. |

Types of Bonds in a Balance Sheet

Bonds are “wiped out” (i.e. not repaid), in the following order

- EQUITY (common shareholders) ← last to be paid, first to be wiped out

- AT1 / Additional Tier 1 (CoCos)

- Tier 2 Capital (subordinated debt)

- Senior Unsecured Bonds

- Secured / Covered Bonds ← paid first, safest

AT1 CoCos

A CoCo is a Contingent Convertible bond.

If the banks capital-ratio (CET1) falls below a threshold, one of two things happen automatically

- bond converts into equity (at bad price for bondholder)

- principal is partially or fully written down to zero → you just lose money

AT1s are designed to absorb losses. Usually the bank can

- skip coupon payments (discretionary, coupon cancellation)

- no fixed maturity date (bank can call them, and not required to)

- if bank is non-viable, regulator can require write-down

They exist because of regulatory requirements (Basel III). Investors still buy them, as yields are much higher!

CDS (Credit default swap)

bps = basis points =

Credit Default Swap (CDS)

A CDS is a financial contract that acts as insurance on corporate bonds. The bond buyer pays a periodic spread to a protection seller. If the bond issuer defaults, the seller pays out the loss.

where is the notional (face value of the debt being insured).

Example: In March 2023, the Deutsche Bank CDS spread rose to bps amid banking sector fears. To insure of Deutsche Bank debt, you paid per year.

If Deutsche Bank defaulted, the seller would pay you the difference between face value and market value of the debt (i.e. if the bonds are worth 6M from the CDS).

Note, in the market, the bps would be higher than the coupon rate, otherwise you would get an arbitrage opportunity which would make it possible to synthetically create a risk-free asset (if the coupon is worth more than the insurance).

Example AIG in 2008. Sold a shit-ton of CDS and sat naked on them hoping the diversification of their CDS would cover, without hedging. So when the entire market collapsed they defaulted.

Correlation between defaults is higher than 50% so this is not a good strategy.

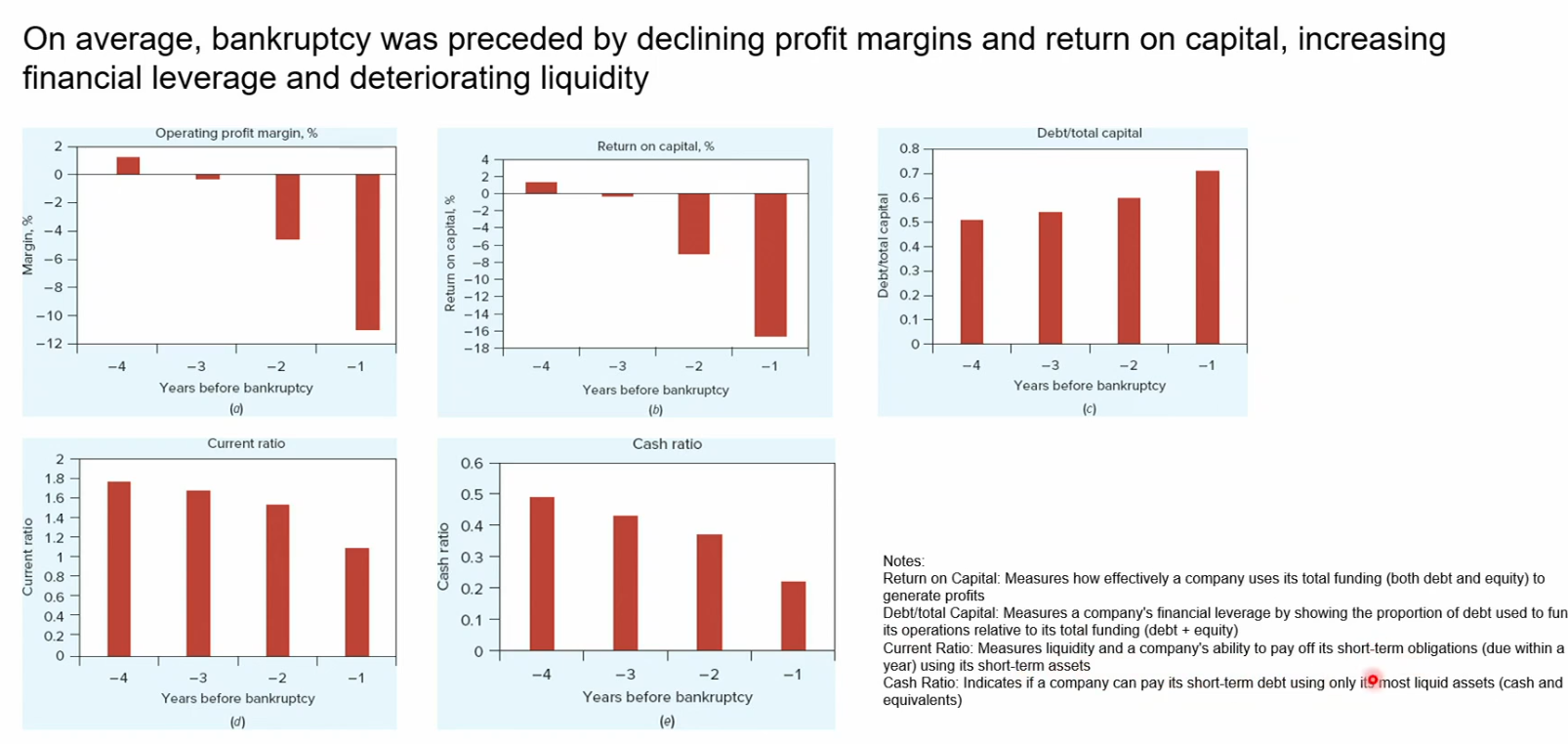

Predicting Default

Altman’s Z-Rating

where:

- = working capital/total assets (Liquidity ratio)

- = retained earnings / total assets (Retained earnings ratio)

- = earnings before interest and Tax (EBIT) / total assets (Asset profitability ratio)

- = market value of equity / book value of total liabilities (Leverage ratio - how much financed by debt vs. equity)

- = sales / total assets (Asset turnover ratio)

Z-Score prediction

A score below indicates impending bankruptcy.

Altman thresholds:

Z-score Interpretation

Z < 1.8 Bankruptcy zone

1.8 – 3.0 Grey zone

Z > 3.0 Safe zone

Examples

Convertible Bond Example

Convertible Debenture — Key Terms

A convertible subordinated debenture is a bond that can be exchanged for a fixed number of shares at the holder’s option. The key quantities are:

- Face value : the par value of the bond

- Conversion price : the per-share price at which conversion occurs

- Conversion ratio : number of shares received per bond

- Conversion value : market value of the shares received upon conversion

The Maple Aircraft debenture has , coupon , conversion price , share price , and market price of face value (so 910$).

- Conversion rate at face value

- Implied Conversion Price (if )

- Conversion Value

The market price () exceeds the conversion value (), which itself exceeds the bond floor (). If market price < conversion value - everyone would convert.

Default-Risk and Risk Premium

If the default-risk is completely diversifiable → investors require no risk-premium.

In that case, the expected return = risk free rate.

Otherwise, we need to discount at expected return rate to find the PV.

Extra

Refinancing

replace debt with new debt (usually to change the terms)

Example

- take out mortgage in 2020 at 7% for 30 years

- in 2024 rates drop to 4%

- you go to a bank → borrow new loan at 4%

- use those proceeds to pay of the 7% in full and now owe 4% instead

In a corporate/merger context

A company has $500M of bonds outstanding at 5%, issued 3 years ago. A private equity firm acquires it. The PE firm doesn’t want those bonds — they have loose covenants, wrong maturity, or the firm wants to put more leverage on. So they:

Raise new debt (say, leveraged loans at a higher rate, but with terms they control)

Use those proceeds to call the existing $500M bonds at the call price (e.g., 102 cents on the dollar)

The old bonds are gone; the new loans replace them

Priority in Default

Even though something is an “unsecured debenture” or a junior unsecured debenture, it doesn’t mean there’s no recourse to getting something back on default → they just have a “general claim”

A secured bond is a bond tied to and secured by a specific asset!

Issuing more bonds pari passu (i.e. at the same rank), dilutes their share and rate of recovery in case of default.

Financial Innovation in Bond markets

- Investor choice: Innovations create securities that satisfy investor preferences. Example: CAT bonds allow investors to earn returns tied to catastrophe risk.

- Regulation and tax considerations: Some bonds are structured to exploit regulatory or tax differences. Example: Eurobonds issued in offshore markets.

- Reducing agency costs: Some bond structures align the interests of shareholders and creditors. Example: CoCos, which convert to equity when capital falls below a threshold.

Debenture Pricing

6% debenture (= yearly) with a 1000 face value pays interest semianually on June 30 and december 31.

Bond is callable at a price of 102% of face value + accrued interest.

If called on September 30th → what amount must be paid?

On september 30th → 90 days since last coupon on June 30th → in total 180 days.

- so we get 90 / 180 of the next coupon.

The semiannual coupon is 6% / 2 = 3%.

So 1.02 * 1000 face value * (1 + 3% * 0.5) = 1035.3