Leasing

Lease = a rental agreement that involves a series of fixed payments from the leasee (user) to the lessor (owner).

- Operating leases: short-term, cancelable lease

- initial lease period is shorter than economic life of the asset

- flexible because they are shorter than the asset’s economic life.

- often includes valuable embedded options

- option to cancel the lease early, renew the lease, upgrade to newer equipment, or purchase the asset at the end of the lease.

- These options reduce the lessee’s downside risk.

- often includes valuable embedded options

- Financial leases: long-term, noncancelable lease

- lease period long enough for the lessor to recover cost of the asset

- Rental lease (full service)

- lessor provides maintenance and insurance

- net lease

- lessee provides maintenance and insurance

- direct lease

- lessor buys the equipment from the manufacturer

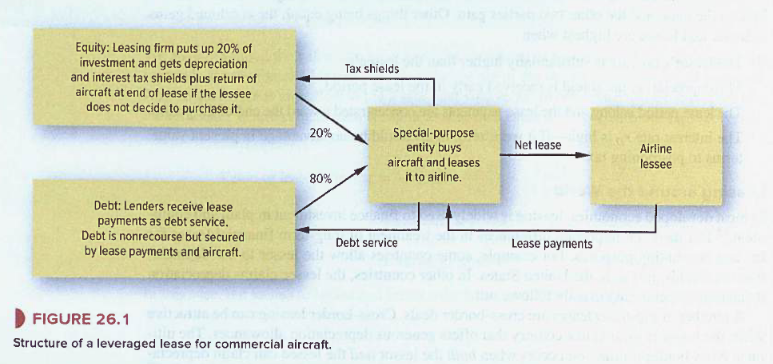

- leveraged lease

- lessor finances the lease contract by issuing debt and equity claims against it

- it’s usually 80% financed by the bank/debt and 20% by the lessor

- sale and leaseback

- lessor buys the equipment from the prospective lessee (capital now, pay in rates)

When the lease is terminated, usually you get the equipment (or whatever you leased).

Differences to a loan:

- non-floating interest = fixed payment for lease

- up to 100% financing usually

- collateral is the thing being leased

Why to lease:

- if you don’t need the asset for full life-span (Operating leases)

- you lease it for a short-term, and usually get maintenance on it, etc…

- the lessor gets extra money

- unrisky, since there’s always the collatoral. Lessee can retain the asset even if in financial distress - since it’s an asset on the balance sheet

Why not to lease - avoids capex costs by going to opex (lease payments instead of outright buying)

- preserves capital, but doesn’t “save” it → makes company look healthier

- often total higher cost since lease costs higher

- leases could be used historically to hide leverage because they were off balance-sheet

Example What happens if a bankrupt lessee affirms a lease? What if it’s rejected

- if affirmed, continues to lease at predetermined rates

- if rejected, asset is returned to lessor

- the lessee then owes: outstanding payments - value of asset

- if the asset is not enough, the lessor has an unsecured claim on the bankrupt firm

Operating Leases

Decision: lease vs. buy

Equivalent annual cost:

—TODO

Buy if the equivalent annual cost of ownership and operation is < best lease rate. Ex: planning to use it for a long time (as lessor needs to include administration costs, etc… in the price).

Note there might be two cases where operating leases make sense even when the company plans to use an asset for a long time:

- lessor is able to buy and manage the asset at lower cost (economy of scale)

- operating leases contain useful options (cancel the lease)

Financial Lease

Decision: lease vs. borrow (borrow = bank loan for purchase)

Financial leases only make sense if company is prepared to take on risks of owning and operating the leased asset (= just another way to borrow money to pay for an asset).

Consequences of lease

- do not have to pay for asset → cash inflow of X$

- no longer owns the asset = no depreciation

- must pay lease for Y years

- lease payments are fully tax deductible

- i.e. they generate tax shields of X$ * 21% tax rate

NPV of leasing vs buying:

initial financing provided (+X$ * tax-rate, because we “get”, i.e. keep, that money) - cashflow from the leasing rates.

- Calculation: Discount the lease cashflows at the after-tax interest rate that the firm would pay on an equivalent loan

is the tax rate. So we discount at after-tax rate .

Note, If you can get a loan with the same cash-flow as the lease in every future period, but a higher immediate cash-flow then you should not lease. ⇐> equivalent to an NPV calculation (if NPV < 0 then borrowing is better)

Calculating value of the lease to the lessor

= negative cashflow at start + discounted cashflow that comes back

NPV when instantly depreciable vs. linearly

The example from the book with Graymare buses has the bus be depreciable instantly, all in the first year.

That’s why the initial positive inflow is only +100 * (1 - 0.21) = 79 and then minus the first lease payment

→ Depreciation all counted in first year

If the asset is however straight line depreciable at a constant x $ per year, we have to include the lost depreciation into the cashflow

→ as money going out!

This annual depreciation tax shield that is lost has to be valued as:

annual depreciation * 0.21 = tax shield lost

and added to the cost.

When does a Lease pay

If tax-rates are the same, it’s a zero-sum game.

Combined gains to lessor and lessee are highest when:

- lessors tax rate is substantially higher than the lessee’s

- depreciation tax shield is received early in the lease period

- lease period is long and lease payments are concentrated towards the end of the period

- interest rate is high → if it were zero there would be no advantage in present value

SPV Leasing Planes

Leveraged Lease

Leasing Accounting

Under IFRS 16 leases have to be recognised on the balance sheet in order to improve transparency and comparability of the balance sheets.

Before, they were off balance sheet → lessee reported neither asset nor liability for future lease payments. → Understated the firms true obligations.

Errors

Lease duration

A lease for 8 years has 8 payments from the lessee to the lessor in total.

Lease cashflow → After Tax

The lease payments also generate a tax shield, so you apply the 0.79 factor to them before discounting.

Note, in year 0, the cashflow is +asset * 0.79 - first_payment

Lease discounting

You discount Years 1-X at ^1, ^2, …, ^(X-1) in total. Year 0 is not discounted.

Calculating Lease Payment (pre-tax) must the lessor charge?

The lessor needs to charge such that NPV = 0.

We first calculate the PV of the cost of the machine (after-tax) and each maintenance payment (after-tax, then discounted at cost of capital).

Assume PV = $210,911

Then break-even pre-tax * (1 - 0.21) = after-tax rent. We need the annuuity (6%, 5 periods) to equal PV.

Annuity due factor = .

- we want the PV today of receiving 1 at the end of each year for n years, with discount rate .

Note: we multiply by (1+r) to offset the 1 discount factor for t = 0.

The formula above is equivalent to .

Annuity factor

For discount rate and periods:

Equivalent Loan

The equivalent loan is a hypothetical bank loan that generates exactly the same after-tax cash flows in each future period as the financial lease.

By comparing the amount of upfront financing provided by the lease (the Year 0 cash flow) with the amount that could be borrowed via the equivalent loan, we can determine whether the lease or borrowing is more advantageous.

If the equivalent loan amount > the lease’s Year 0 cash flow, the lease has negative NPV (borrowing is better).

If the equivalent loan amount < the lease’s Year 0 cash flow, the lease has positive NPV (leasing is better). The difference equals the NPV of the lease.

Calculating Lease NPV vs. Buying

For the lease vs. buy calculation, we calculate the cashflow of leasing, and add the lost depreciation tax shield onto the yearly cost.

CF_0 = + 19800 - 2300 * ( 1 - 0.21) = 19800 - 1817

This is the asset price saved, minus the first after tax lease payment.

Each year after, you pay the after-tax lease payment, and lose the depreciation tax shield

Annual Outflow = 2300 * (1 - 0.21) + 19800/9 * 0.21 = 2279

where 19800/9 * 0.21 is the annual depreciation tax shield, which we lose → thus we add it to the cost

To calculate the PVIFA we do the following:

Note, 6.32% = . This is the after-tax borrowing rate.

PVIFA(6.32%, 9 years) =

Then PV = 2279 * 6.6958 = 15259.73

Therefore NPV = CF_0 - PV = 17983 - 15259.73 = +2723.27 > 0

Present Value Interest Factor of Annuity (PVIFA)

For discount rate and periods, the present value interest factor of an annuity is the multiplier that converts a constant periodic payment into its present value today:

It gives the present value of receiving n$ periods.

Note: this gives you the value of 9 payments, 1 at the end of each year so 9 total.

→ first payment extra as year 0 Cashflow

Example: A 9-year annuity at after-tax borrowing rate :

So a stream of $2,279 per year for 9 years is worth 2{,}279 \times 6.6958 \approx \15{,}260$ today.

Annuity Due Factor

If the first payment occurs immediately (at ) rather than at the end of the first period, multiply the ordinary annuity factor by :

This offsets the one-period discounting shift: each payment arrives one period earlier, so each is worth a factor more.

In lease NPV calculations the annuity due applies when the first lease payment is due immediately. However, the Year 0 payment is usually handled separately as a direct cash flow, and the remaining or payments are discounted as an ordinary annuity starting at .