Managing Risk & Understanding Options

1 Why Manage Risk?

Risk management doesn’t always add firm value. Two reasons it may not:

- Hedging is a zero-sum game — gains cancel losses across counterparties.

- Investors can hedge themselves (DIY alternative), so firm-level hedging is redundant.

Still, firms face real risks that justify hedging: cash shortfalls, financial distress, agency costs, FX fluctuations, political instability, weather.

2 Insurance

Insurance

Transfer of a firm’s non-diversifiable hazard risk to an insurer (or risk pool). The expected loss is shared across many policyholders; each pays a proportional premium.

Example: \1\text{bn}1/10{,}000$ storm risk per year. Expected loss per member of a 10,000-firm pool:

An insurer won’t necessarily offer this at \100\text{k}$ because of:

- Administrative costs

- Adverse selection — riskier firms are more likely to buy insurance

- Moral hazard — insured party takes more risk

Correlated losses (e.g. all platforms in the same region) amplify the insurer’s true exposure far beyond any single firm’s probability.

Catastrophe Bond (CAT Bond)

A bond whose coupon/principal payments are reduced if industry-wide (or issuer-level) insurable losses exceed a threshold. Allows insurers to transfer tail risk to bond investors.

Moral hazard note: Issuer-level triggers incentivize overcommitment to high-risk books; industry-level triggers do not.

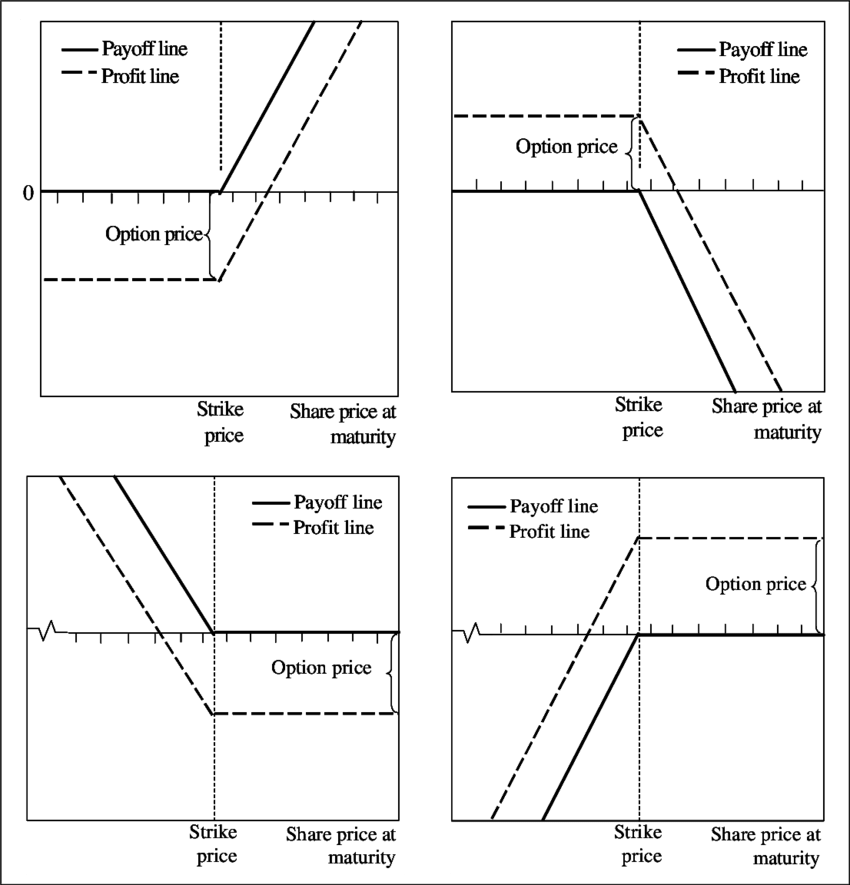

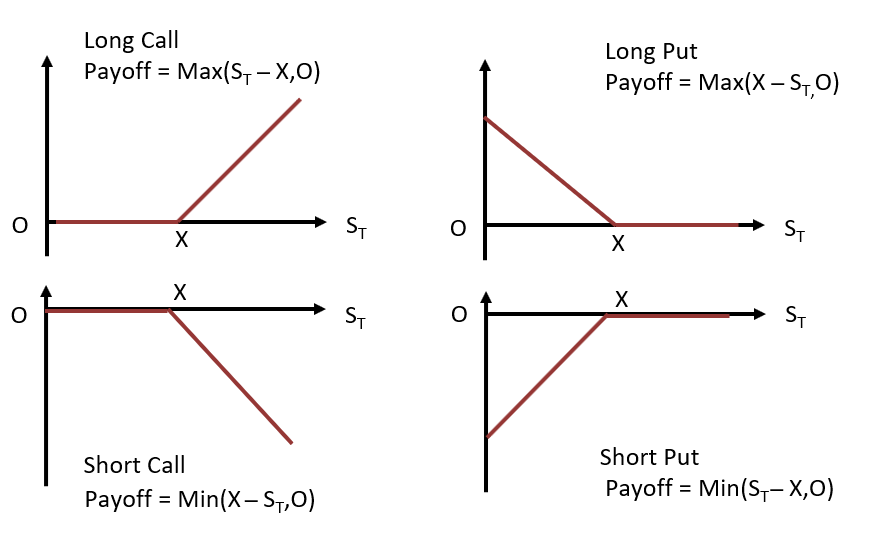

3 Options

Option

A contract giving the holder the right (not obligation) to buy or sell an asset at a specified exercise price (strike) within a specified period, for a premium.

- Call option: right to buy

- Put option: right to sell

- American: exercisable any time up to expiry

- European: exercisable only at expiry

Payoff profiles (ignoring premium), is strike, is exercise price:

| Position | Payoff at expiry |

|---|---|

| Long call | |

| Long put | |

| Short call | |

| Short put | |

| Payoff = (exercise price) - strike |

The seller of a call faces unlimited loss potential — they must deliver at regardless of how high rises.

**Example (Amazon, Jan 2020, S_0 = \1{,}830K = $1{,}830$146.20$1{,}830 + $146.20 = $1{,}976.20$.

Put-Call Parity Formula

(Value of Call) + PV(EX) = (Value of Put) + Shareprice

PV(Ex) = Present value of exercise price = ex / (1 + r_d)

Intuition: C - P = S - PV(Ex)

Buy Call and sell put = buying share and borrowing money

→ Buying call - put is a synthetic forward = locked in buying stock at price Ex on date T which is same as buying now + borrowing

- if Strike > Exercise → Call - Ex

- if Strike < Exercise → Put - Ex

if you buy the stock and loan you also have exactly Shareprice - Repay Ex

Options value with Volatility

Options written on volatile assets are worth more than options written on safe assets!

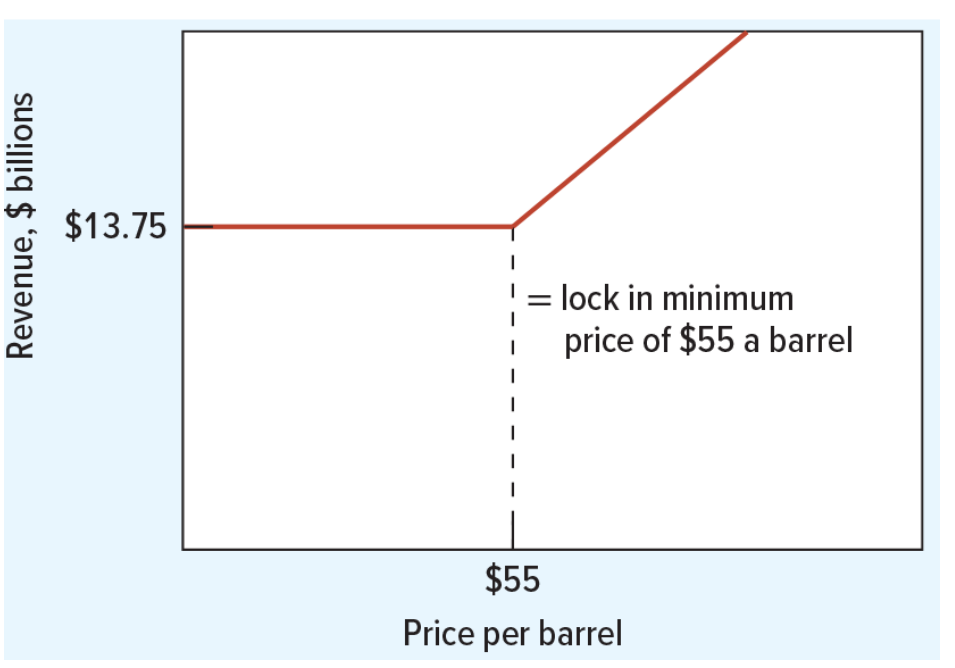

3.1 Reducing Risk with Put Options

An oil producer selling 250M barrels can buy put options (strike K = \55$13.75\text{bn}$. Revenue profile:

- If S_T < \55$55$13.75\text{bn}$

- If S_T > \55$: sell at market, upside retained

When to manage risk and Hedge

Only if there is no fluctuation of cost with rising/falling market conditions → ex: expensive R&D program

- an oil company that wants to invest doesn’t need to hedge as in high-price times there’s less demand anyways

some companies allow managers to hedge risks in an internal market

- synergies / counterparties stay in company

- managers don’t accidentally trade with exposure

4 Forward & Futures Contracts

Forward Contract

A bilateral agreement to buy/sell an asset at a specified price on a specified future date. Traded OTC; settled at maturity.

Futures Contract

Like a forward, but exchange-traded and marked to market daily. Gains/losses settled continuously.

Basis risk: arises when the hedging instrument is not perfectly correlated with the asset being hedged.

- imagine oil price rising in kansas where supplier is

- but they bought new-york futures (where price doesn’t rise)

Then they lost money, as their futures didn’t pay out difference of rising costs (cannot buy from new-york, only local)

Example (Arctic Fuels/Northern Refineries): Arctic (short on oil) and Northern (long, producing oil) enter a forward at \2.40$/gallon for 1M gallons in January. Both lock in price regardless of spot moves. Each creates an offsetting position to their natural exposure.

4.1 Pricing Financial Futures

For equity index futures:

where is the risk-free rate and is the dividend yield.

Example (CAC, 6-month): , , :

4.2 Pricing Commodity Futures

Net Convenience Yield (NCY)

The net benefit of holding the physical commodity vs. a futures position. When NCY , futures trade below spot (backwardation). When NCY , futures trade above spot (contango).

Example (WTI, Feb 2022): S_0 = \124F_{1\text{yr}} = $92.50r_f = 0.3%$:

Market in backwardation — immediate scarcity from Ukraine invasion expected to ease over time.

5 Interest Rate Risk

forward interest rate is the extra rate of return you earn by extending a loan from one period to two.

Forward Interest Rate

The rate agreed today for a loan starting in the future, implied by the yield curve:

Example: , :

We know

Thus

Suppose you want to loan \frac{1.000.000}{1.10}$ discounted for 2 years at 12% and lending for 1 year at 10%, letting interest accumulate at 10% until you hit exactly 1M after 1 year.

But there’s an easier way: FRA (forward rate agreement)

need $ 50M for 6 months in 3 months

buy 3 x 9 (three against nine) month FRA with a bank

If interest rates rise, bank pays difference on your 6 month loan (extra you would have to pay) and if they fall you pay the diff to the bank

What would be paid: 10M

- at 5% for 6 months = . so 250k

- At 6% it would be 300k

Thus without the FRA you would have lost 50k. Now we take this difference (payable at the end of the 6month period) and discount it by the actual interest rate paid on the loan

- 50k / (1 + 0.06 * 180/360) = 50k / (1.03) = 48.54k

That’s what you get paid out.

interest rate futures

you can also buy futures on interest rates via treasury futures.

if price of treasury bonds (is almost interest rate, so some basis risk left) falls , profit from sale of futures should offset lower price of bonds that company sells in the future

(cost of carry relationship for asset that throws off income while you hold it)

is current yield (coupon / price). If you buy future you earn interest but lose out on coupon payment → price of future lower by that amount.

6 Swaps

6.1 Interest Rate Swaps

Interest Rate Swap

An agreement where one counterparty pays fixed cash flows and receives floating (or vice versa) on a notional principal. No exchange of principal; only net interest payments flow.

Example (5-year fixed-to-floating, 6% vs SOFR, notional \66.67\text{m}$):

- Year 1: SOFR → bank pays \4\text{m}$3.33\text{m}$0.67\text{m}$

- Year 2: SOFR → net payment

At creation, swap NPV . If rates subsequently rise to , the PV of three remaining \0.67\text{m}$ net payments is:

6.2 Currency Swaps

Currency Swap

Exchange of fixed cash flows in one currency for fixed cash flows in another. Allows a firm to issue debt in a familiar market and swap the proceeds into the desired currency.

A currency swap works as follows:

- exchange principals (A gives 3M CHF to A) at a fixed exchange rate (day spot price)

- Pay interest over duration of loan (at daily rate)

- Exchange principles back (at original rate) → independent of current spot price

Thus there is no risk of price moving anymore.

Example (Possum Co.): Issues \10\text{m}$ USD notes at 6%, swaps into EUR 8m at 5%. Net cash flows are entirely in EUR — FX exposure eliminated.

7 Setting Up a Hedge

7.1 Duration Matching

To hedge interest rate risk on a fixed-income asset, issue offsetting debt with the same duration, not just the same PV.

Example (Potterton Leasing): 20-year annuity lease, \2\text{m/yr}r = 10%= 7.5$ years:

If interest rates rise → PV goes down - your asset (2M a year. If rates rise, that money is “worth more” i.e. you can get more from it. Whereas your repayment is still fixed 2M for loan. (Opportunity cost!)

But Issuing \17\text{m}\approx 0$.

Calculating Duration (Bond or Lease)

For the rate and the number of years and the payment at time the duration is:

Why duration Matching? We want to have the asset and liability to have the same sensitivity to moving interest rates. They might have the same maturity, but due to timing of the cashflow, might have drastically different durations.

If the durations are matched, losses/gains due to small interest rate changes will be offset by losses/gains in the liability.

Dynamic Hedging

Some hedges need to be actively “maintained” and re-calibrated.

7.2 Hedge Ratios & Basis Risk

To hedge Asset A using Asset B, sell units of B per unit of A:

(the hedge ratio) is estimated by regressing historical price changes of A on B. Residual unhedged risk is basis risk.

Example (wheat farmer): Regression of farmer’s price on Kansas City futures gives → sell 0.8 futures contracts per unit of wheat held.

I.e. wheat futures are not perfectly correlated to the wheat price the farmer actually gets.

Beta beta is just delta, but for B = market index.

You need to hedge by .

8 Derivatives & Speculation

Speculators are attracted by the leverage derivatives provide, and their participation helps keep markets liquid. However, speculative positions can cause large losses. Two precautions:

- Monitor positions regularly — don’t be taken by surprise.

- Only speculate when you have a comparative advantage (informational edge) that puts the odds in your favour.

Insurance

Insurance companies cannot diversify away market or macroeconomic risks

- generally used to reduce diversifiable risk and find other ways to manage macro risk

→ insure specific risk usually

Extra

A long term option is known as a LEAPS (Long term equity Anticipation Security).

Option Tricks

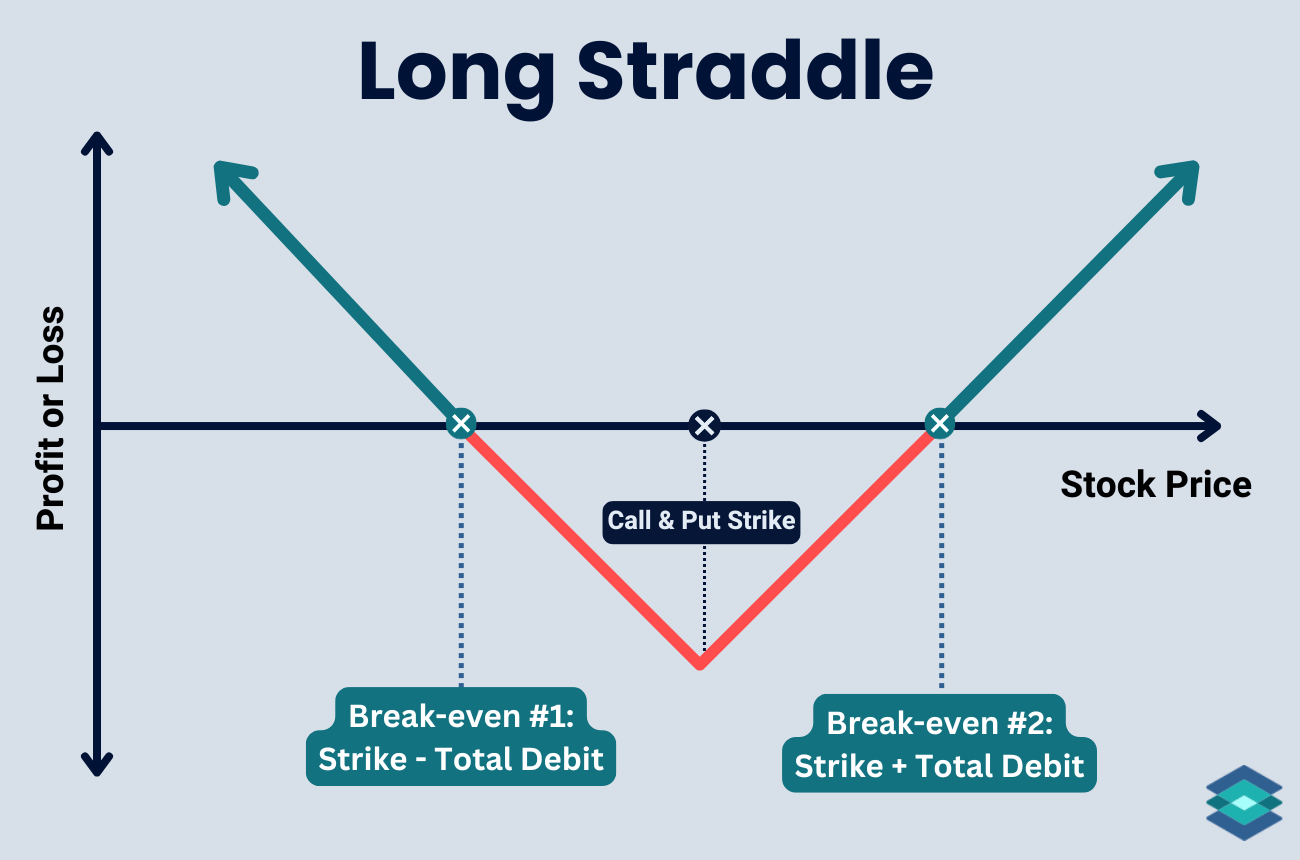

Straddle V-shaped payoff, comes from buying call and put at same exercise price

good if volatility is high

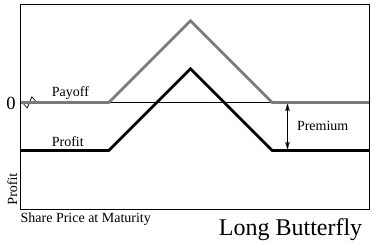

Butterfly Inverted V-shaped payoff

maximum payoff when the stock is near the middle of the exercise price → low volatility

Obtained by buying call at X, selling 2 at X + d and buying call at X + 2d

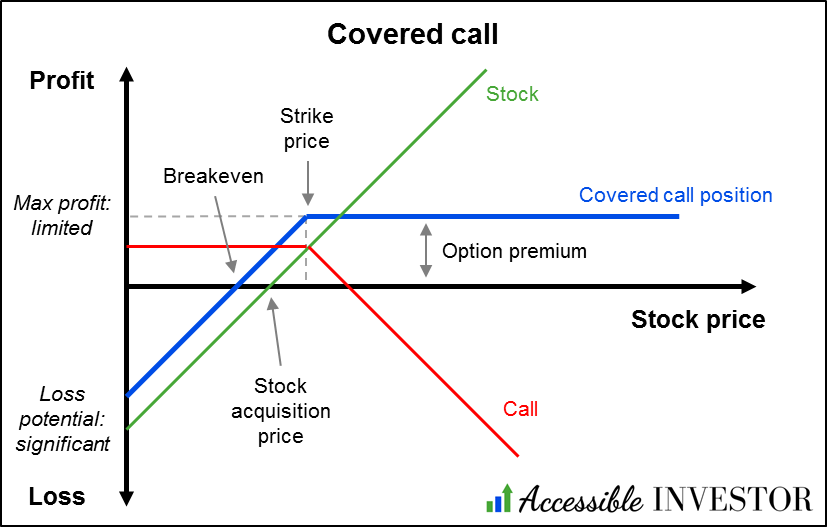

Covered Call

Hold a long position in an asset and sell a call on it. You get immediate income, but cap upside.

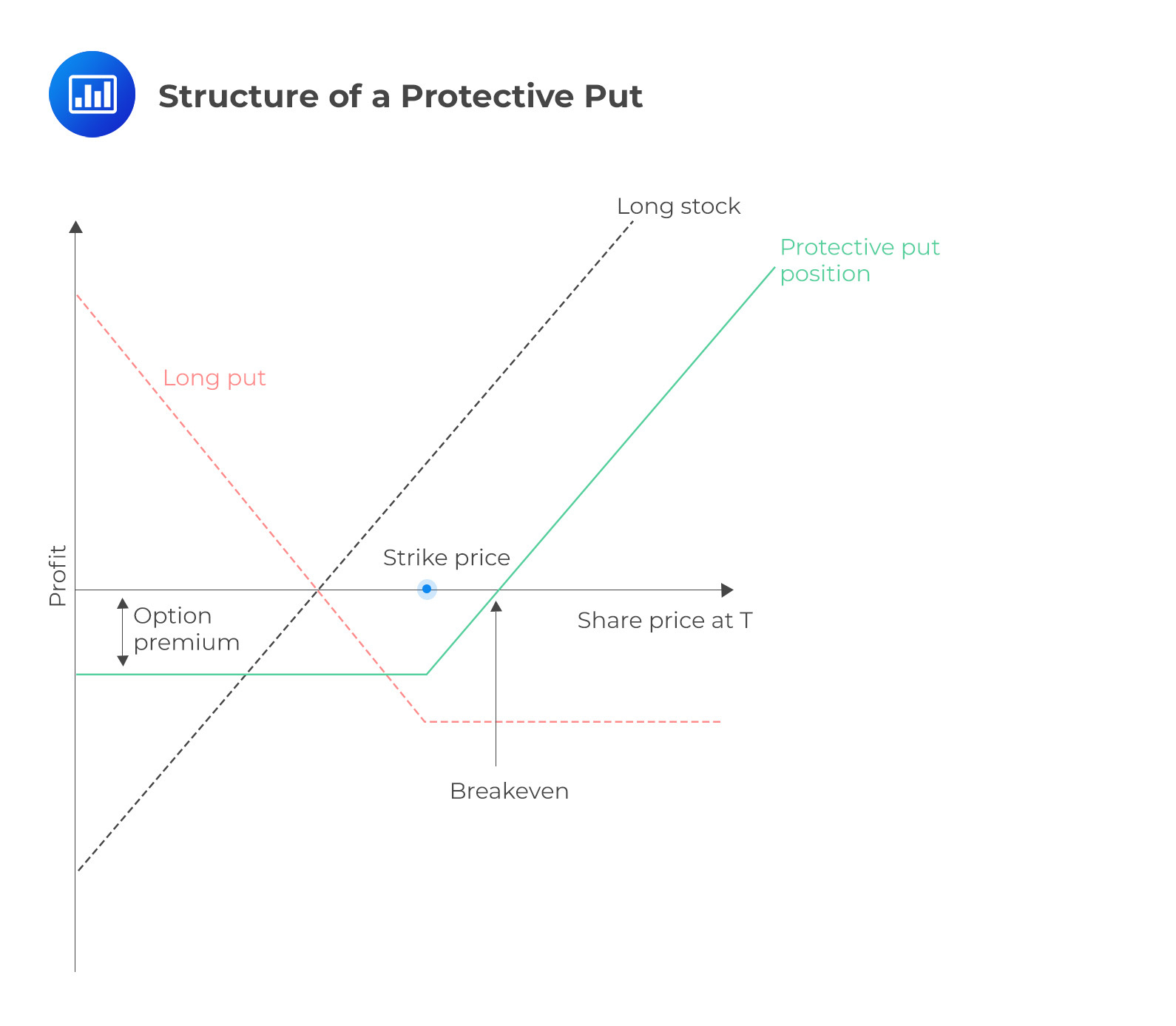

Protective Put

You hold a long position and buy a put option on it → protects downside.

Cost is the option premium

Ex: mexican government on oil prices

Non-Arbitrage for Implied Forward Interest Rate

Forward rate is the interest rate that would make an investor indifferent between

(i) lending for 2 years at 12% and

(ii) lending for 1 year at 10% and then reinvesting for the second year at the forward rate

1.10 * (1 + forward rate) = 1.12

Interest Rate Swap

At initiation → NPV always 0

If rates rise by 1% on a 10M notional for 5 years.

The loss is 4.751% (duration of swap is approx 4.5 years due to coupons), thus loss is 475k

DIY a risk-free bond using Options

By buying a stock, selling a call at that price and buying put at current stock price, you can get a flat payoff curve.

Due to efficient market pricing, you get a risk-free bond.

Call > put

Environmental Derivatives

Short Sale

A short sale of a stock gives you payoff -S at expiration

-S = C + -Pv(Ex) - P

Lower / Upper Bound of European Call Option

The lower bound is max(0, S - PV(Ex))

The upper bound is ⇐ S

Precautions for company trading derivatives

- Do not be taken by surprise, monitor positions regularly.

- Place bets only when you have a comparative advantage.