5.1 Foreign Exchange (FX)

5.1.1 Spot Trade

Spot price = instantaneous price. But then it’s actually delivered 2 days later. (or you pay up).

it’s BASE/QUOTE where

- base is what you’re buying/selling

- quote is currency you’re paying with or receiving

ex: EUR/USD = 1.5. One euro costs 1.5 dollars

note: unit of EUR/USD = usd/eur → it’s the dollars you have to pay per euro

So if silver costs 500 Euros per ounce and 750 dollars

cross-rate

EUR/USD * USD/JPY = EUR/JPY

there is the spot-rate if you want “immediate” delivery.

Then there is also the forwards market:

51.2 FX: Forward

If you know in advance, you could lock in a rate via a forward. But then you lose upside if one currency goes up.

Also note, the forward rate is spot price * the interest rate differential (i.e. opportunity cost of converting now).

If USD rates > EUR rates → USD is weakening faster than EUR.

Thus forward rate for EUR/USD (number of USD per EUR) will be higher than spot = more dollars per euro in the future.

5.1.3 Interest Rates & Forward Prices

Forward Premium and Discount

Let be the spot rate and be the forward rate, both quoted as units of foreign currency per 1 unit of home currency. The annualised forward premium/discount on the foreign currency over a period of years is

- If the result is positive, the foreign currency trades at a forward premium (expected to appreciate).

- If the result is negative, the foreign currency trades at a forward discount (expected to depreciate).

Note the quoting convention matters: because and are expressed as foreign per home, the ratio captures the change in the foreign currency’s value. Reversing numerator and denominator gives the premium on the home currency instead.

Example: The Brazilian real spot rate is BRL/USD and the 3-month forward rate is BRL/USD. The annualised forward discount on the real is

The real is at a forward discount of per year. Equivalently, the dollar is at a forward premium of .

ALWAYS CALCULATE ANNUAL PREMIUM/DISCOUNT!

To see concretely what this means: at spot, USD buys BRL. In the forward market, USD buys BRL — so a holder of reals needs more reals to buy one dollar in 3 months. The real has weakened forward.

Covered Interest Rate Parity (CIP)

Let and be the risk-free interest rates in the home and foreign country respectively, over the same horizon as the forward contract. Then in the absence of arbitrage,

Equivalently, the forward premium on the foreign currency equals the interest rate differential:

Proof (by arbitrage): If the forward traded at the same price as today

- Borrow $1,000 in the US at 4%

- Convert to reals at spot, invest in Brazil at 8%

- In one year, collect your 8% return

- Convert back to dollars at the same rate, repay your 4% loan

- Pocket the 4% difference — risk free

High Interest Rate ↔ Forward Discount

A currency with a relatively high interest rate trades at a forward discount; a currency with a relatively low interest rate trades at a forward premium.

5.1.4 Worked Example

Dollar loan:

The rate of interest on 1-year dollar deposits is . At the end of the year:

RUR loan:

The current exchange rate is RUR / USD . For \1{,}000$ you can buy:

The rate of interest on a 1-year RUR deposit is . At the end of the year:

- You don’t know the exchange rate in 1 year’s time, but can fix today the price if you sell your RURs forward.

- The one-year forward rate is RUR / USD .

- Selling forward, you receive:

Both strategies yield exactly USD — the higher RUR interest rate is fully offset by the forward depreciation of the ruble, consistent with covered interest rate parity.

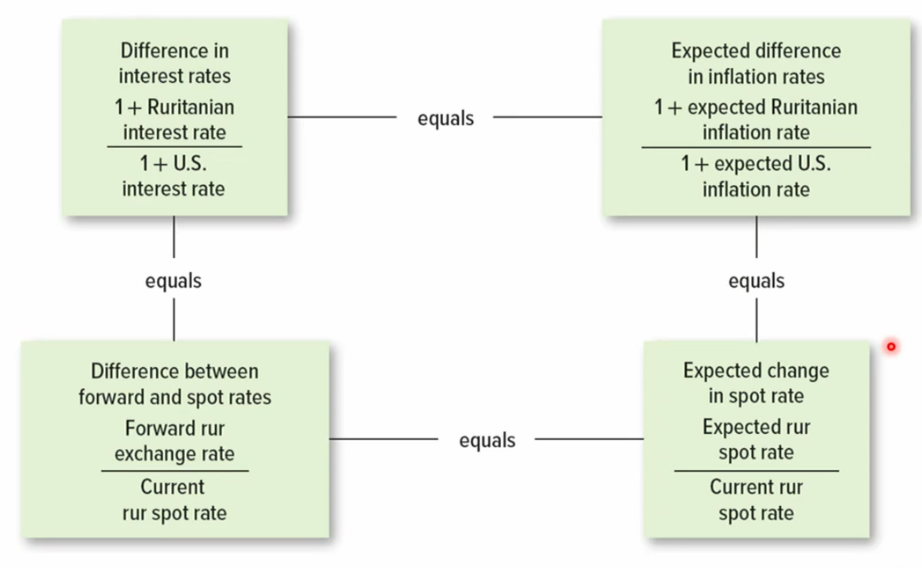

5.1.5 Exchange Rate & Inflation

Interest Rate Parity

If a currency is expected to be more prone to inflation than another, we expect it’s spot exchange rate to be higher in the future.

The market makes sure of this through arbitrage opportunities if not conserved.

In general the following holds: higher interest rate ←> higher inflation rates for a country.

Forward Premium and Changes in Spot-Rates

if risk = 0, then we would expect forward fx rate = future spot price.

So if rur/usd 1-year forwards trade at 55, then we would expect the spot in one year to be 55.

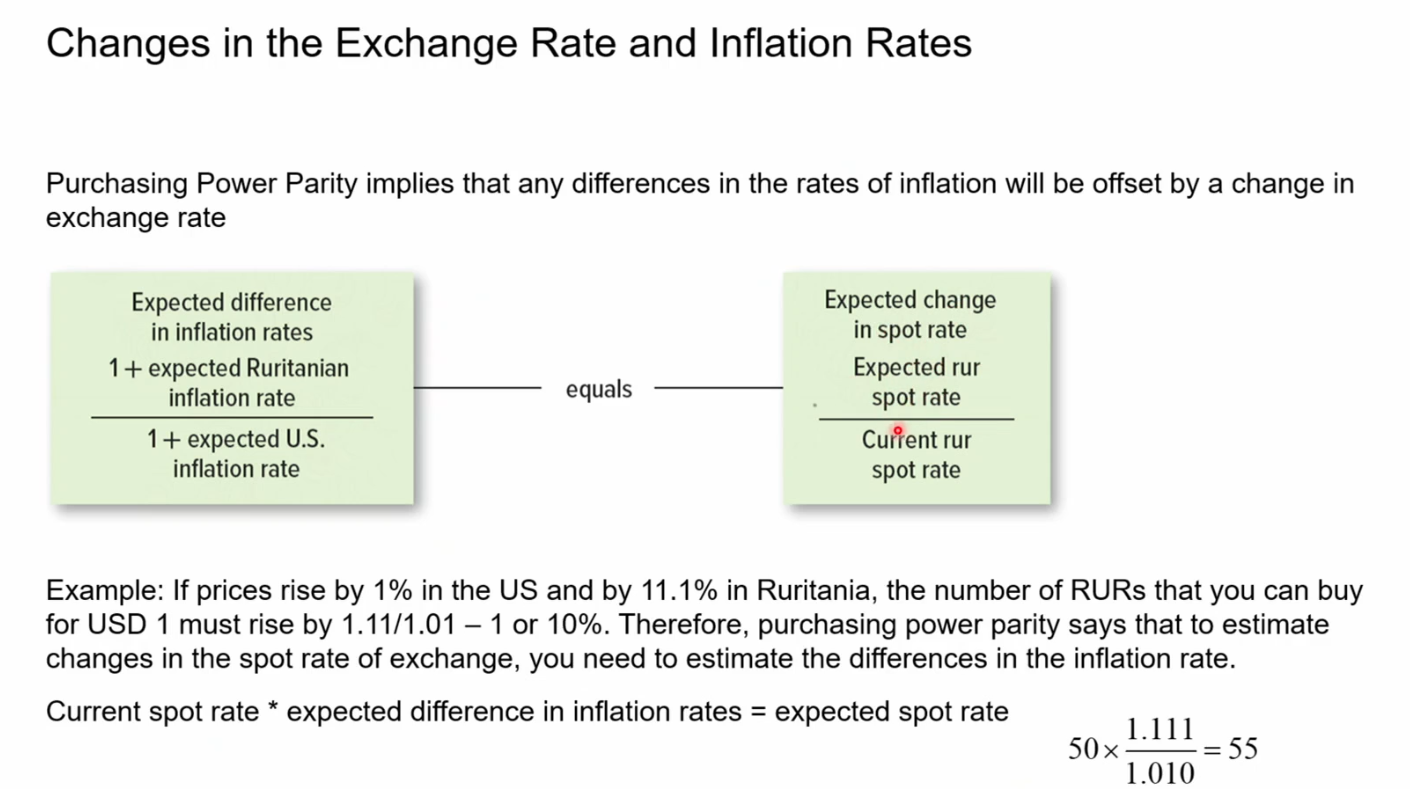

Changes in FX-Rate and Inflation Rates

PPP (purchasing power parity)

PPP stipulates that

Note: In a sentence: “Changes in the spot exchange rate should reflect differences in inflation rates between two countries.”

otherwise there would be an arbitrage opportunity.

If prices rise by 1% in the US and by 11.1% in Ruritania → RUR/USD would rise by .

Inflation adjustment

RUR/USD is how many dollars one rur costs.

Then if is Ruritanian inflation and is US inflation, the forward price is:

Note: the fx-rate and rates are inversed, as RUR/USD is usds one rur costs. So RUR/USD = amount of dollars / amount of rurs something costs.

Thus we need to adjust the dollars (numerator) by the dollar rate, and the rurs by the rur rate (denumerator).

Thus to estimate the changes in the spot-rate of exchange, you need to estimate differences in inflation rates.

Interest and Inflation

The real interest rates in both countries must be the same.

So real expected interest rate = (1 + nominal) / (1 + expect inflation) - 1

is equal in both countries.

5.2 Exchange Risk and International Investment Decisions

Transaction Exposure and Economic Expose

Transaction Exposure: If we know we get X USD in Y years, we need to hedge against the exchange rates moving.

Economic Exposure: If the USD falls in value, to compete we will have to offer lower prices → this means we need to sell USD forward.

Investing Overseas

Roche invests in new plant in the US

Calculate the NPV of the project in dollars. Then convert those dollars at the spot rate to CHF to get the NPV in CHF.

This works out to be exactly the same as buying a forward hedge for each future cashflow and discounting in CHF. Because you can hedge, you can ignore the outlook of the currency and focus only on > 0 NPV

Required Return on Foreign Investments

Roche invests in US → shareholders like this because this diversifies their exposure. One CHF more in switzerland is just more of the same.

Thus they would be willing to accept lower rate of return from a US investment than US investors would demand on the same.

beta of swiss index is correlated at 0.8

then: required return = swiss interest + (beta * swiss market premium)

so for 7.4% risk premium:

required return = 4 + (0.8 * 7.4) = 9.9%

where US investors would require more.

CAPM

Capital Asset Pricing Model (CAPM) is a framework for pricing risky assets and estimating expected returns. The core idea: investors need to be compensated for (1) the time value of money and (2) the amount of systematic risk they bear.

Expected return = + market_risk_premium

where the market risk premium = market-rate - risk-free-rate

Fisher Equation

real interest rate = (1 + nominal) / (1 + inflation)

For two countries this ratio should be the same! → This is the fisher effect (international fisher effect).

Extra

Futures Price

where is the interest rate (ex: 0.07 = 7%) and are the dividends (if paid out at end of year).