Cash-in, Cash-Out and Working Capital

Example:

- pay out extra $10M in cash dividend

- decreases cash by $10M

- decreases WC by $10M

- Receive $2.5k from customer (from previous sale)

- increase cash by $2.5k

- no change (was already under receivables)

- Pay $50.0k previously owed to suppliers

- decrease cash

- but was already booked under current liabilities → balances out

Working Capital Management

Working Capital is the difference between a company’s current assets and current liabilities.

Working Capital Requirement

operational concept → how much capital a business needs to tie up to fund it’s operating cycle (gap between paying for inputs and receiving payments from customers)

which simplifies to

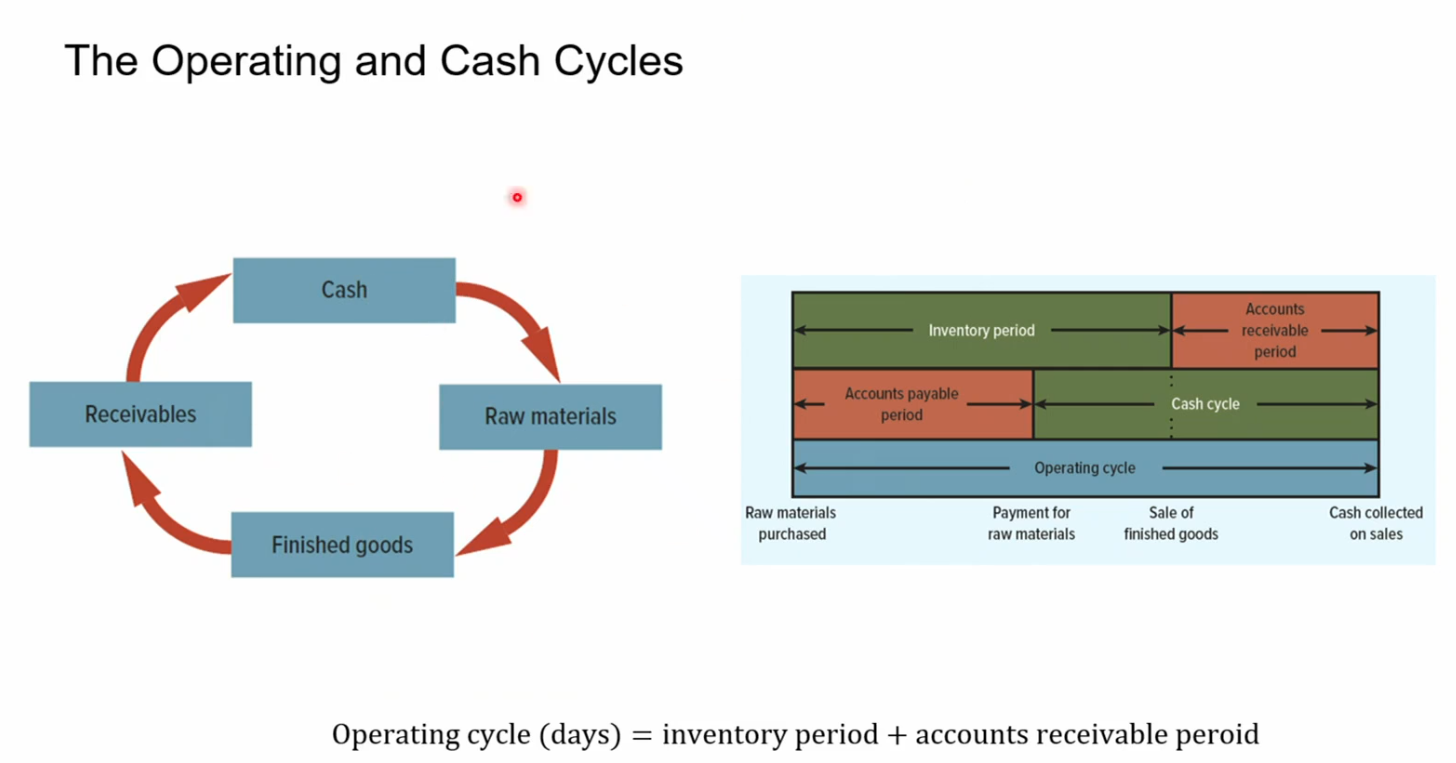

Operating cycle: total time

Cash Cycle

cash cycle = inventory period + accounts receivable period - accounts payable period

measures how long it takes for a company to convert it’s cash investments in inventory back into cash from sales.

= net number of days your own cash is locked up in the operating cycle

Interval between firm’s payment for raw materials and collection of payments from customers (i.e. the time they’re out of cash).

- average inventory period =

- average receivables period =

- average payment period =

Important KPI (amazon has had negative CC for years → collect from customers before you pay suppliers)

Link to WCR

The CashCycle and WCR are two sides of the same coin:

- WCR = how much cash is tied up in the cycle (a stock, in €/$)

- CCC = how long cash is tied up in the cycle (a duration, in days)

You can derive WCR from CC: WCR = Revenue x (CC / 365)

- daily revenue = revenue / 365

- how long that cash is tied up

if revenue doubles → WCR also doubles → too much cash tied up / increases cash requirements

Example Effects on the Cash Cycle

-

Customers are given a larger discount on cash transactions

- Effect: CCC shortens ↓

- A discount incentivizes customers to pay immediately (cash) rather than on credit. This reduces the receivables period (DSO) — you collect cash faster instead of waiting 30, 60, 90 days.

-

The firm adopts a policy of reducing accounts payable

- Effect: CCC lengthens ↑

- Reducing accounts payable means the firm pays its suppliers sooner (or takes on less payable balance). This decreases the payables period (DPO).

Inventories

- raw materials

- work in progress

- finished goods (should be empty → sold to clients)

Goal → minimise cash tied up in inventory

Tools to minimise inventory:

- just in time

- order size:

- increase order size → order number falls (more per order) → order costs decline

- however: increase in order size → increase average inventory amount

- strike a balance

- increase order size → order number falls (more per order) → order costs decline

Financial Planning

Free-Cash-Flow Model

Operating Cash Flow = Depreciation + After-tax interest + Net income

Note we add After-Tax interest back because FCF is computed assuming all equity financing

FCF = operating cash flow - CapEx

- CapEx = investment in fixed assets

- we also include Investment in working capital as CapEx

model for valuation that estimates the value by forecasting how much cash it generates after accounting for capex, then discounting those cashflows back to today.

Planning

Plan for at least 5 years, accurate forecasting

But not too deep into details, it’s “art”

Horizon Value Model

Given a “horizon value” of a firm, say 10x the earnings in 2026 under all equity financing, we can calculate the PV

PV = (FCF year 1) / cc^1 + (FCF year 2)/ cc^2 + … over the years + (FCF year t + Horizon value) / cc

where FCF is the free cash flow of that year and cc is the cost of capital

Accounts Receivable Management

- Trade Credit: Receivables from one company to another

- Consumer Credit: receivables from customers

Five questions for management

- How long time for customers to pay bills?

- Prepared to offer Cash discount for prompt payment?

- How do you determine which customers likely pay their bills?

- How much credit are you prepared to extend each customer? (play it safe vs. risk acceptance)

- How do you collect the money when it comes due?

- what about reluctant payers or deadbeats?

Terms: ex: “2/10 net 31”

- 2: percent discount for early payment

- 10: number of days discount is available

- 31: days until the bill is due (no discount)

Credit Analysis: determine likelihood customer pays their bills

- credit agencies (Dun and Bradstreet is largest one)

- financial ratios

- ask bank for a “credit check” on your customer

Credit Policy: standards set to determine the amount and nature of credit to extend to customers

Credit Scoring: What your lender won’t tell you

- extending credit gives you probability of profit → not guarantee

- still a chance of default

- denying credit guarantees neither profit nor loss

Collection Policy: procedures to collect and monitor receivables

Factoring: Arrangement whereby a financial institution buys a company’s accounts receivable and collects the debt

When to pay

If you have 5/10, net 60 and you decide not to take the discount, what interest rate are you getting on your loan.

effective annual interest = (1 + )^{365 / extra days credit} - 1

so in our case = (1 + 5/95)^{365/50} - 1 = 45.4%

When to grant credit

If the expected gain from granting credit > 0

EV = p * PV(REV - COST) - (1 - p) * PV(COST)

customer pays with prob p and defaults with probability (1 - p).

But if there is the chance of repeat order → you might lose good customer if you don’t offer credit

- if margin of profit is high → easier to give credit

- otherwise, be sparing

You can also outsource the collection to a factor, which is a business that just deals with getting paid. You may even get 70-80% of the order value financed in advance, with pre-agreed interest.

Cash Management

→ cash does not pay interest

- Move money from cash into short-term securities

- usually less than one year notes

- “sweep programmes”

- pooling

Forecasting cash needs

- Forecast sources of cash

- largest usually payments by firm’s customers

- Forecast the uses of cash

- Calculate whether the firm is facing cash shortage or surplus

- either raising or investing cash

for 1, we need to see how long on average until customers actually pay their receipts → until then the receipts are not cash but assets receivable

for 2, estimate payments of accounts payable, increase in inventory, labor/admin costs, capex and taxes

for 3, we take the difference to calculate how much extra cash we need from short-term loans

to do this, see:

Developing a short term financial plan

we can either:

- bank loan (borrow money)

- stretching payables (put off payments of bills)

→ stretching payables is often costly (even if no ill-will) as suppliers may offer discounts for prompt payment

ex: if 5% discount is lost and we pay next quarter = equivalent to annual loan at 20% interest rate (4 * 5% = 20% → usually would need geometric average but it’s short enough).

Pitfalls: the models should be adjusted to account for fixed costs, depreciation and taxes, etc…

- percent-of-sales methods ignore the existance of fixed costs

- many models ignore depreciation and taxes

- models generally produce accounting numbers rather than financial cash flows

Money Market Investments

You say that a x-month bill is issued at a y% discount.

This means that the price (in %) is p = 100 - (x/12) * y.

To annualise, you then do (100 - p) / p which gives you the x month rate. Then you do .

Extra

External Capital Required

(CFO = cash flow from operations for planning)

- Increases in receivables USE cash;

- decreases in inventory RELEASE cash;

- increases in payables RELEASE cash.

External capital required = ΔNWC + ΔFixed Assets + Dividends − CFO

Operating CF

Operating CF = Depreciation + After-tax interest + Net income

FCF = OCF - Investment working capital - investment fixed assets

Sustainable Growth Rate & Plowback

Plowback ratio = retained earnings / net income

proportion of net income that the company retains and reinvests back into the business → rather than paying out dividends

SGR = plowback * ROE

→ Maximum growth rate the firm can maintain without increasing leverage

Internal Growth Rate The maximum growth rate a firm can achieve using only retained earnings — no external financing at all.

The SGR is the maximum growth rate achievable while maintaining a constant debt/equity ratio.

EOQ

Economic Order Quantity: Order quantity that minimises total inventory costs → balances orders against holding costs

EOQ = √[(2 × 10,000 × 50) / 4] = √250,000 = 500 units.

Banker’s Acceptance

A bankers’ acceptance is an unconditional promise of a bank to make payment on a

draft when it matures.

The acceptance is in the form of the bank’s endorsement (“acceptance”) of a draft drawn against that bank in accordance with the terms and conditions of a letter of credit issued by the bank.

→ the bank is essentially an escrow, but a “tradeable asset” gets created here

These are traded at a discount.

→ pays fixed value at maturity

- because not matured, investors buy it for PV

Bankers’ acceptances have their origin in international trade transactions.

→ Cross-Border trade

- seller ships goods but is afraid bank won’t buy

- buyer pays but is afraid seller won’t ship

- → bank assures, and seller can even sell the BA on the market to get money immediately