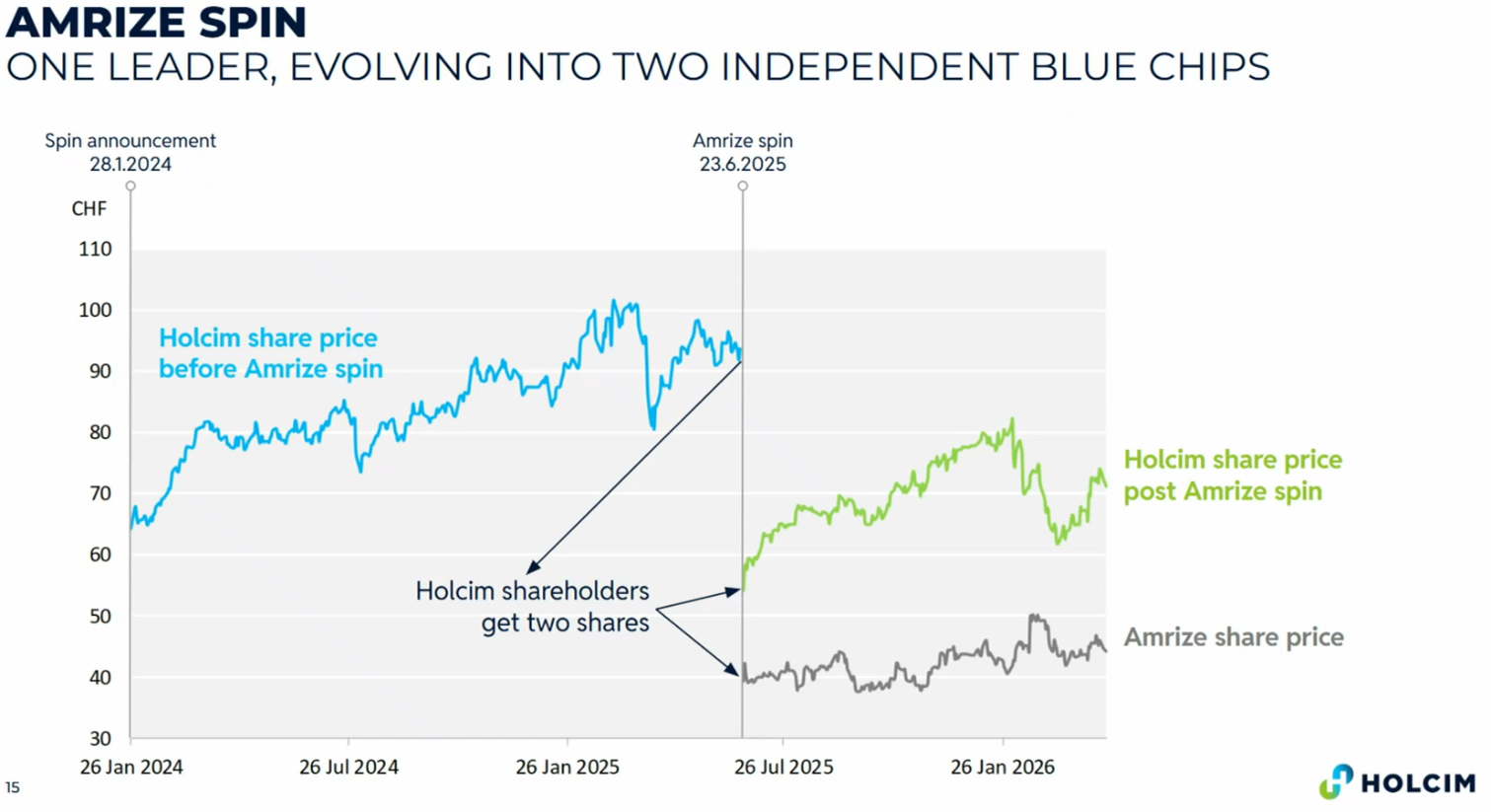

Spin-Off

Holcim spun off it’s North-American business to create a new and independent, publicly traded company called Amrize.

- one amrize share per holcim share held

- amrize listed at NYSE and Swiss stock exchanges

Reasons:

- pure focus on north-american customers → decentralised business model

- cement is not transported, produced locally and so they operate locally

- pure US$ based, tailored capital structure

- environmental regulation in US vs. Europe → too big a difference

- Create a distinct investment profile for investors

- have choice to invest only in US

- main factor

- EV / EBITDA ratio was worse for Holcim than US peers

- means that EV / EBITDA ratio can be better in US

- Also increased EV / EBITDA in the Europe

- EV / EBITDA ratio was worse for Holcim than US peers

Spin transaction → separate 1 share into 2

- holcim valuation dropped → US business is out

(different slide) If you take out amrize share value historically, you can see big increase in value when amrize spin was announced and executed +132.5%

How to separate the business

Spin out the business, want to separate the debt ($8.4 bn) from Holcim into Amrize.

- there were bonds, you cannot simply move them

- amrize (North american business) had debt against holcim

So, two transactions

- Amrize raised new bonds (for $3.4 bn) on 2. April 2025

- injected in 4 tranches (2, 3, 5, 10 year maturity)

- this was supposed to pay back the debt to Holcim

- Bond exchange

- offered choice to bond investors: want to stay with holcim or move to amrize

- done before spin

- par-for-par exchange to transfer certain USD bonds to Amrize

- Fall-away guarantee from holcim that falls away upon successful spin closing

- offered choice to bond investors: want to stay with holcim or move to amrize

Other treasury activities

- secure liquidity

- bridge facility (financing to cover bond exchange and issuance)

- ensure amrize has liquidity for daily ops, 2bn

- revolving credit facility

- commercial paper program → issue commercial papers (short term)

- secure rating

- rating evaluation / assesment with S&P and Moody’s to determine the upper and lower threshholds for BBB+/Baa1 credit ratings for Holcim pre- and post-Amrize spin

- Treasury team

- build new team that is operational from day 1

How to Issue a bond

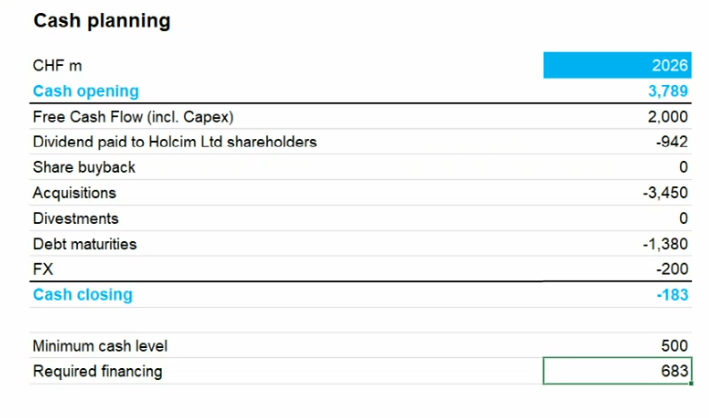

First: Detailed cash planning to understand what you need.

Understand cash-”opening” here → what you start off with and then “cash-closing” what is left.

Then you are left with 683M to get to the $500M minimum (set arbitrarily).

How do you place such a bond?

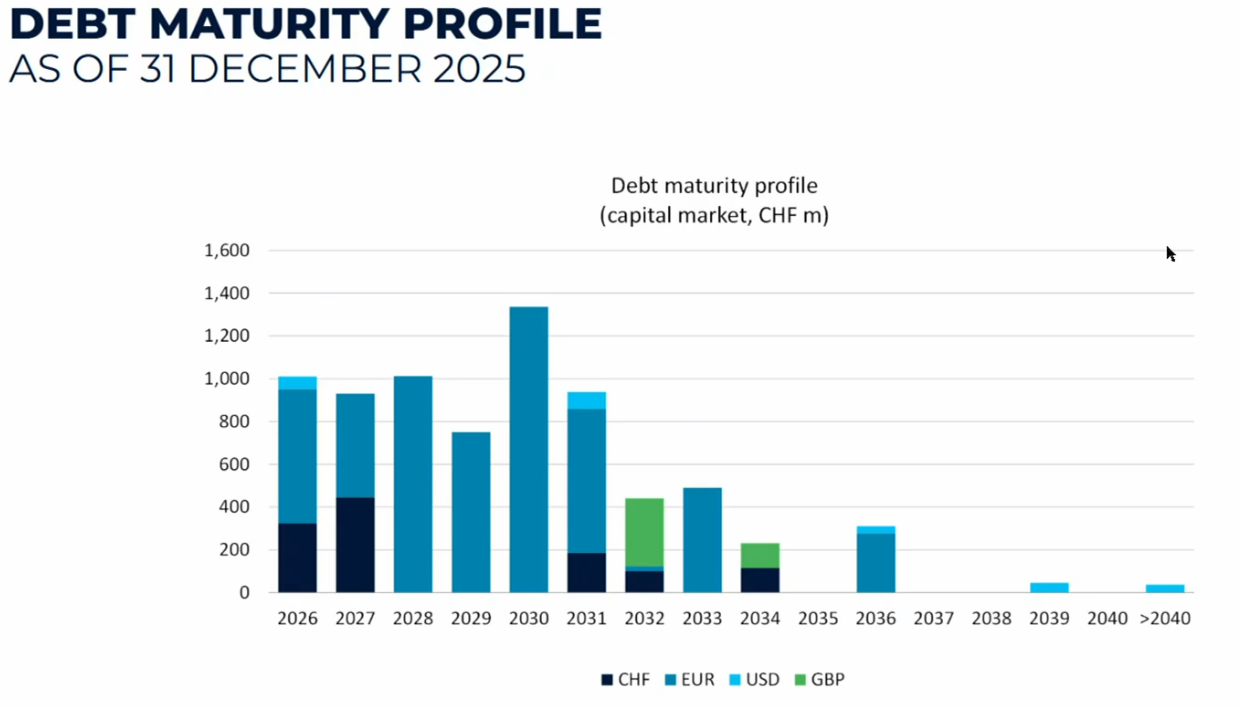

- do not have a “peak of bonds”, keep the distribution even!

- distribute currency even

This is the distribution → $1bn per year maturing is “reasonable” for them

A large part of Holcim’s balance sheet is from Capital Markets → not from banks but bonds. The average bond maturity is 7 years.

- longer maturity → lower refinancing risk

- lengthening maturity profile in low interest rate periods

- → reduce interest expenses in high-interest periods

- long maturities not always available (especially for lower rated companies)

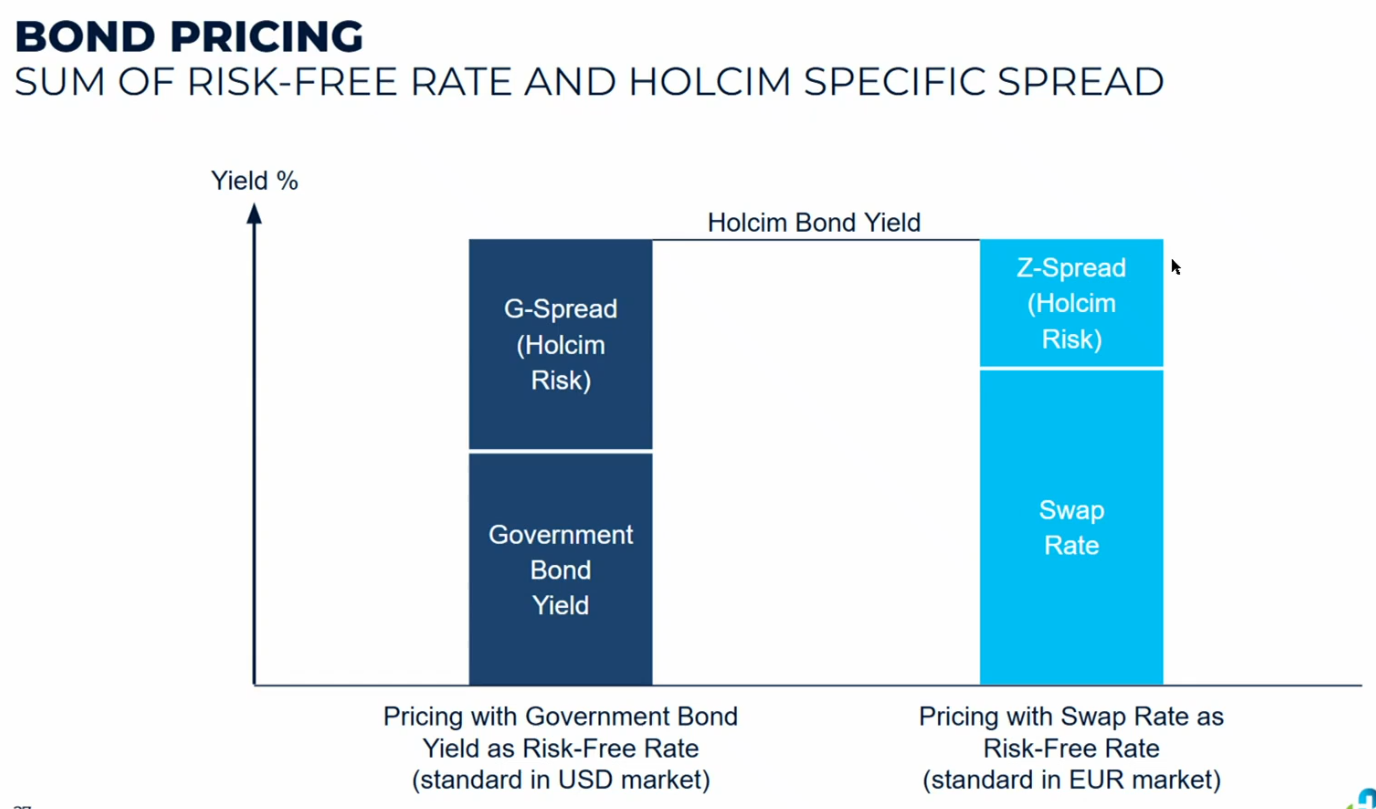

Bond Pricing:

- priced with “spread” above government bond yield

Re-offer Yield

The re-offer yield is the yield-to-maturity at which an underwriting bank sells (“re-offers”) a newly issued bond to final investors. It is set as

where the swap rate is the risk-free benchmark and the spread compensates investors for the issuer’s credit risk.

The swap rate is the risk-free rate and spread is the “extra” on top investors demand.

- swap rate = paying this rate fixed per year for X years is fair exchange for receiving floating short-term rates (SOFR/LIBOR) for the same X years

- the fixed rate you receive in exchange for giving up your floating payments

- Note, it’s not risk-free because of no risk → rather because it’s the “naked” lending rate between banks → void of any risk calculations

Re-offer Price

The re-offer price is the price per 100 face value that investors pay. It is mechanically derived from the re-offer yield — the unique price at which the discounted cash flows equal the investor’s required return.

= PV of all cashflows, discounted at re-offer yield

The two are not independent: given the yield, there is exactly one consistent price.

Example: Holcim issued a CHF 475m, 6-year bond on 7 June 2010 with a 2.375% annual coupon, a swap rate of 1.403%, and a spread of 105 bps.

- The re-offer yield is .

- The re-offer price is the present value of all cash flows discounted at this yield: .

→ We discount at re-offer yield because it is the investor’s required return

- Since the coupon (2.375%) < required return (2.453%)

- bond trades at a small discount below par: investors pay less upfront to make up for the below-market coupon

No investor would buy a “fresh” bond at 80bps → if there are already bonds trading on the market for that rate

- so you have to give a slight discount to attract capital