UBS has two sides

- Global Banking (GB) → private information from clients, etc…

- global markets → quant, trading, etc… (public information)

US is biggest market, biggest M&A fees

M&A

There are 2 reasons:

- revenue reasons

- accelerate growth, enter new markets, diversify

- better products (see Pharma Acquisition)

- cost reasons (cost synergies, avoid new competitors, increase purchasing power)

- economies of scale

- vertical integration

There are two main legal classifications:

Merger

“Legal” transaction

Two companies combine all assets and liabilities.

one will survive → other is incorporated in.

Merger is more difficult regarding tax (than acquisition)

- international → exit tax

Acquisition

two ways:

- stock purchase (easy legal transaction)

- asset purchase (acquires explicit assets)

- only assumes liabilities of the target that have been specifically determined

- lots of legal precision required

Note under public M&A rules, either a merger or public offer is more advantageous (approval threshold, interloper risk when doing an acquisition)

Other Classifications

- nature of target (public, private, public subsidiary)

- geography (international, national)

- strategy (bolt on, transformational)

- type of consideration (cash, stock, mix)

- process type (bilateral discussion, limited auction, broad auction)

- pro-forma ownership (merger of equals, outright acquisition)

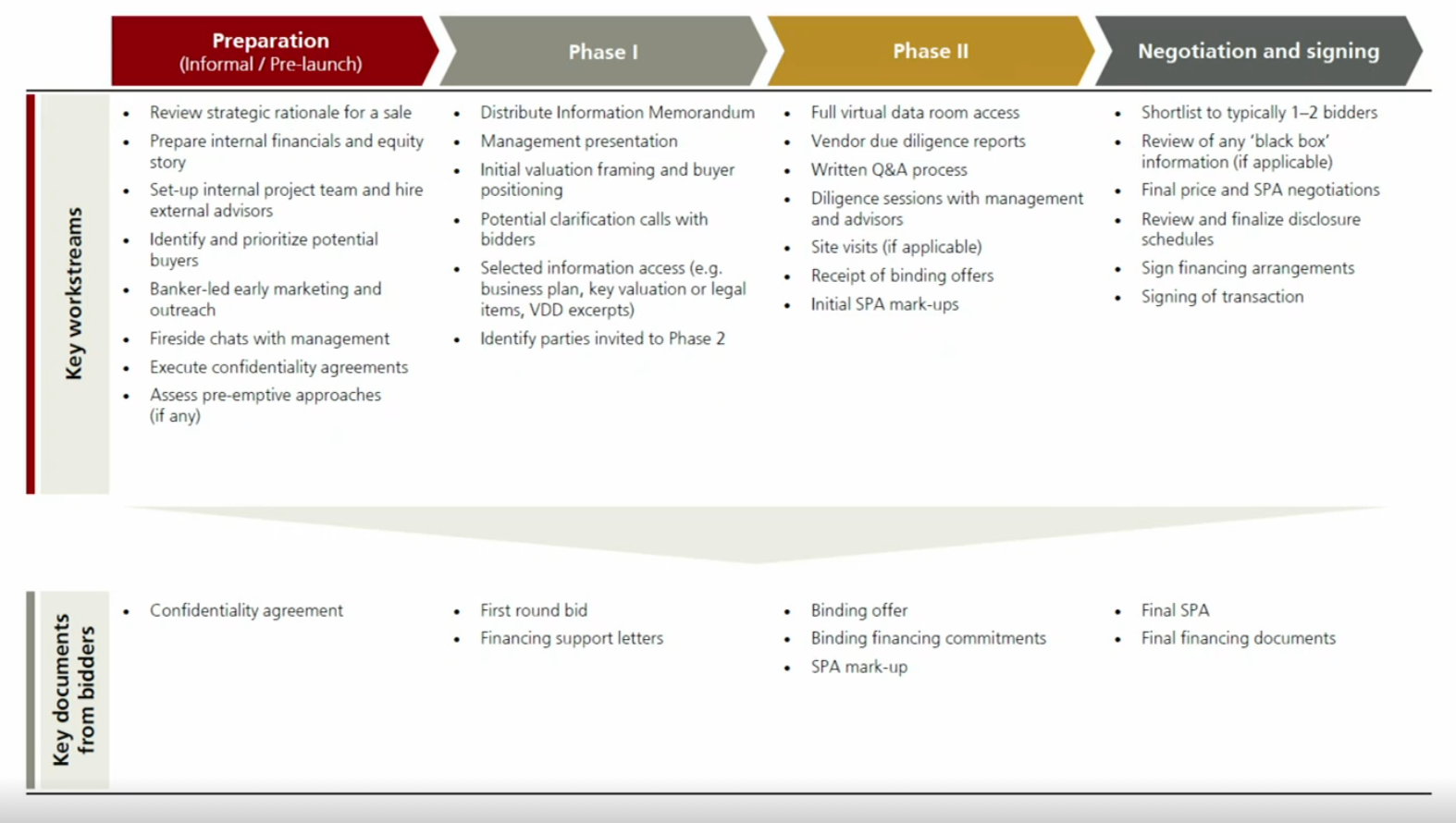

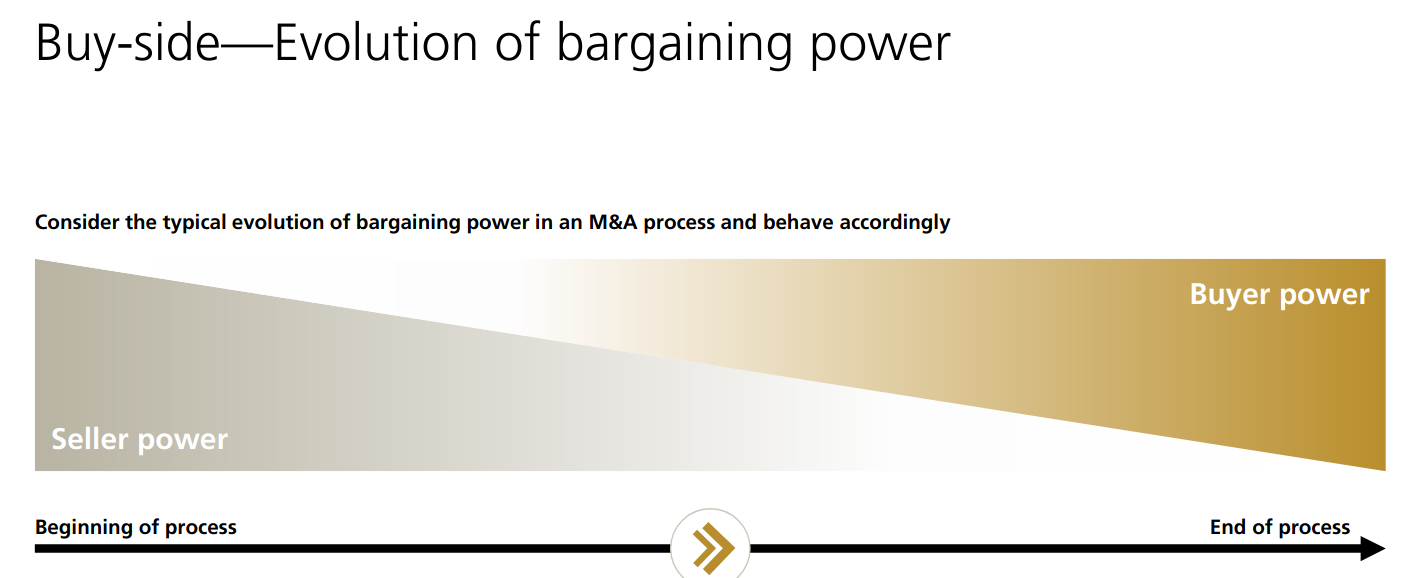

M&A sell side process

very careful of how to approach this:

- if you’re selling, why? is something wrong?

→ careful framing planning

Due Diligence Report → large document from external vendor, commissioned by external vendor

recently: change of more casual approach → more preparation, informal approaches

Foreign Players in US → not easy. You almost have to have a local bank, otherwise investor pool will ask questions

- US banks are cohesive in not helping out foreign banks

- US banks don’t compete on fees → almost “monopoly”

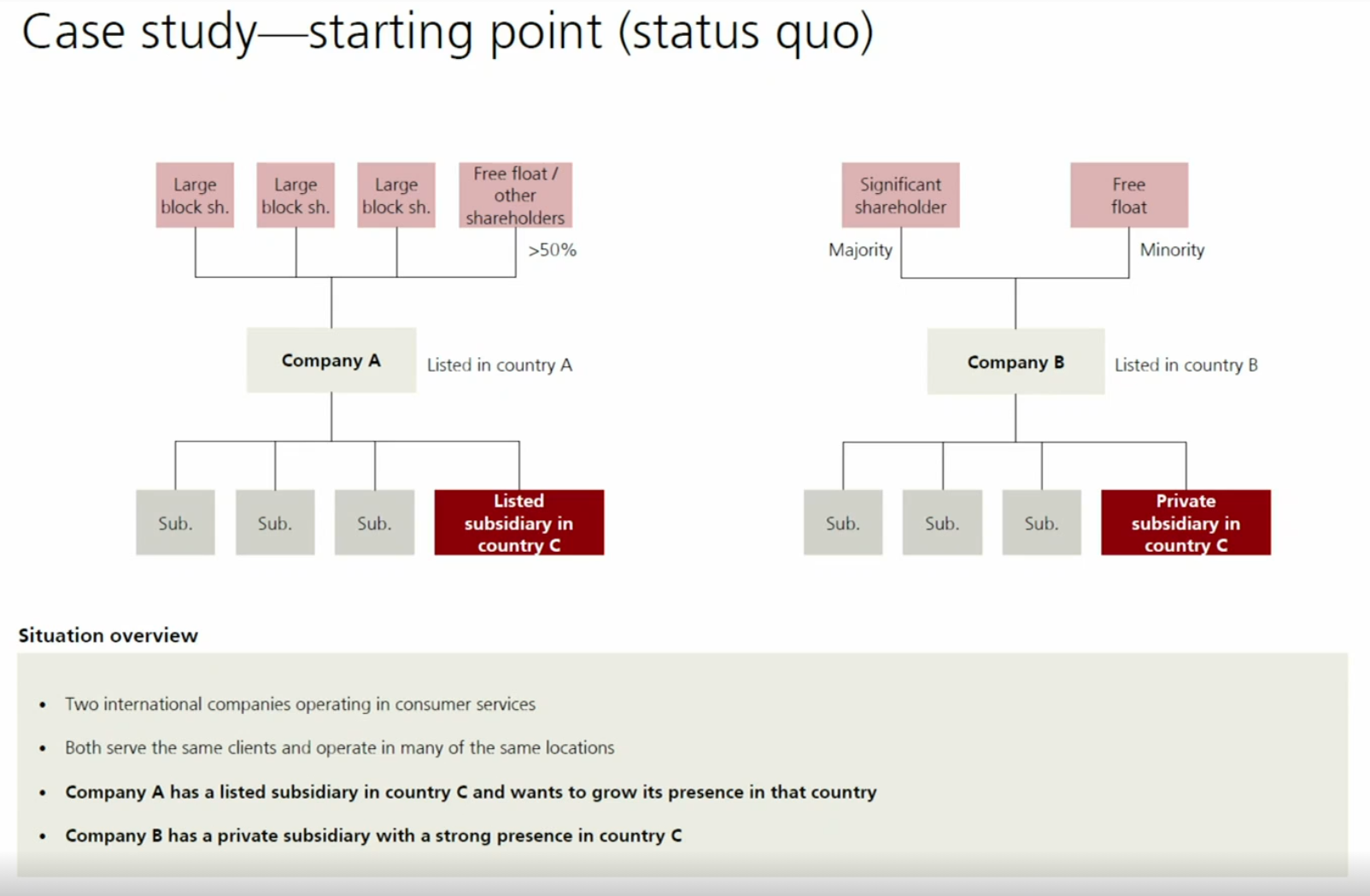

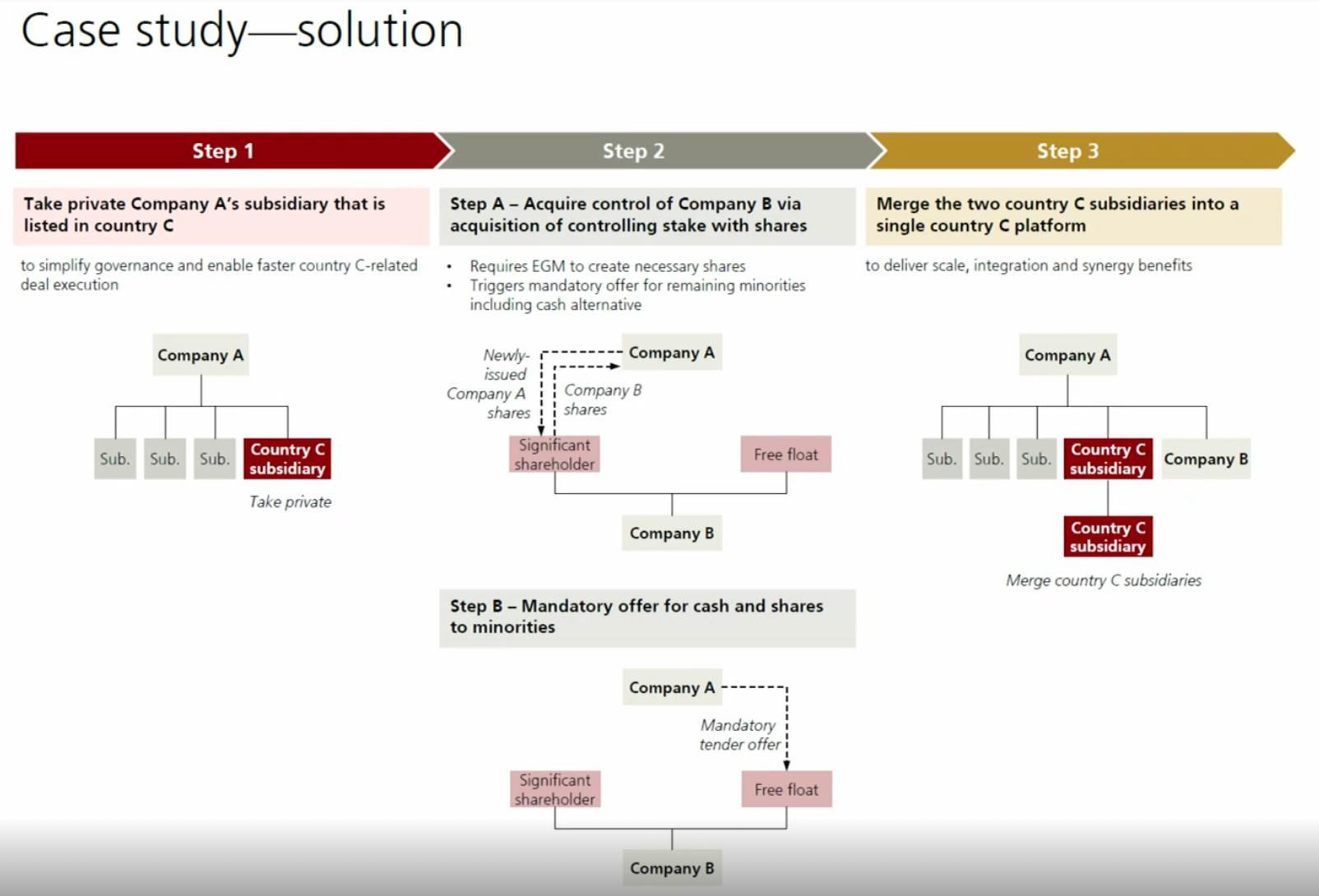

Case Study

adjacent spaces, not same area but same clients, etc…

two shareholders (private, public)

Note:

- B’s subsidiary is very valuable (majority of value of B)

- B’s subsidiary also much larger than A’s presence in the country

Qs:

- integration, competition issues, legal ramifications

- who should be the buyer (A, subsidiary, other)?

- → they decided listed company A should buy

- who should be target (B, subsidiary)

- → company B now

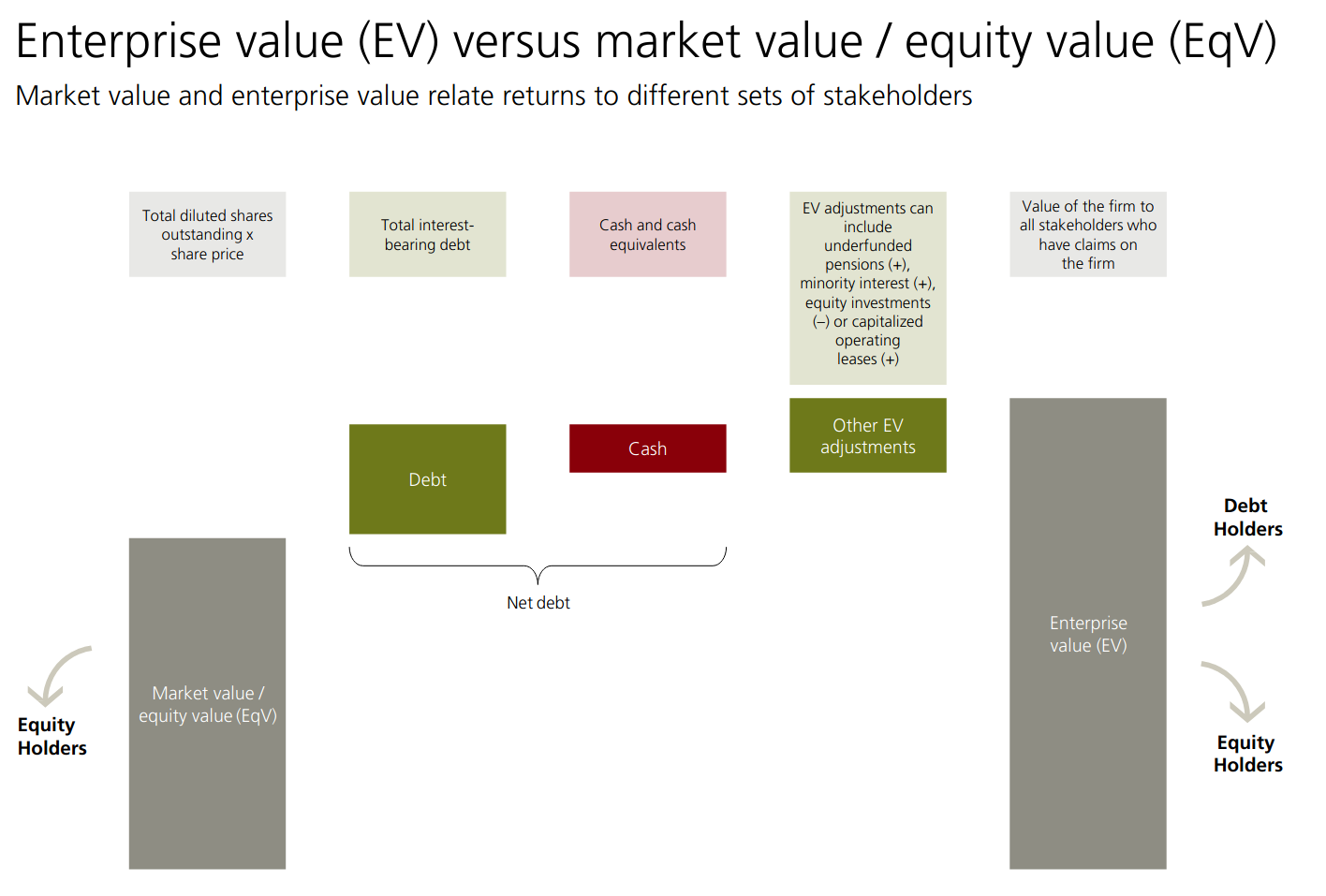

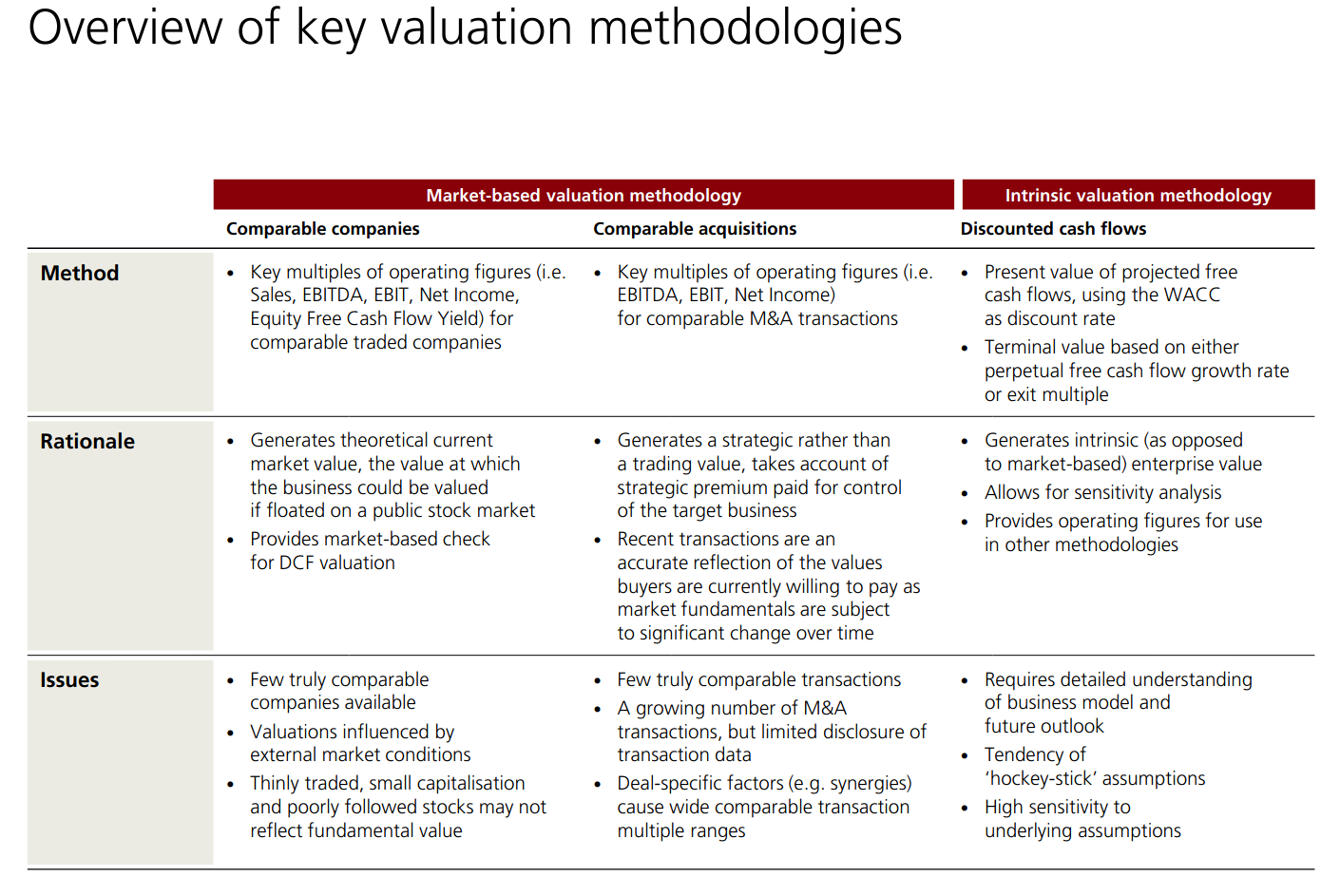

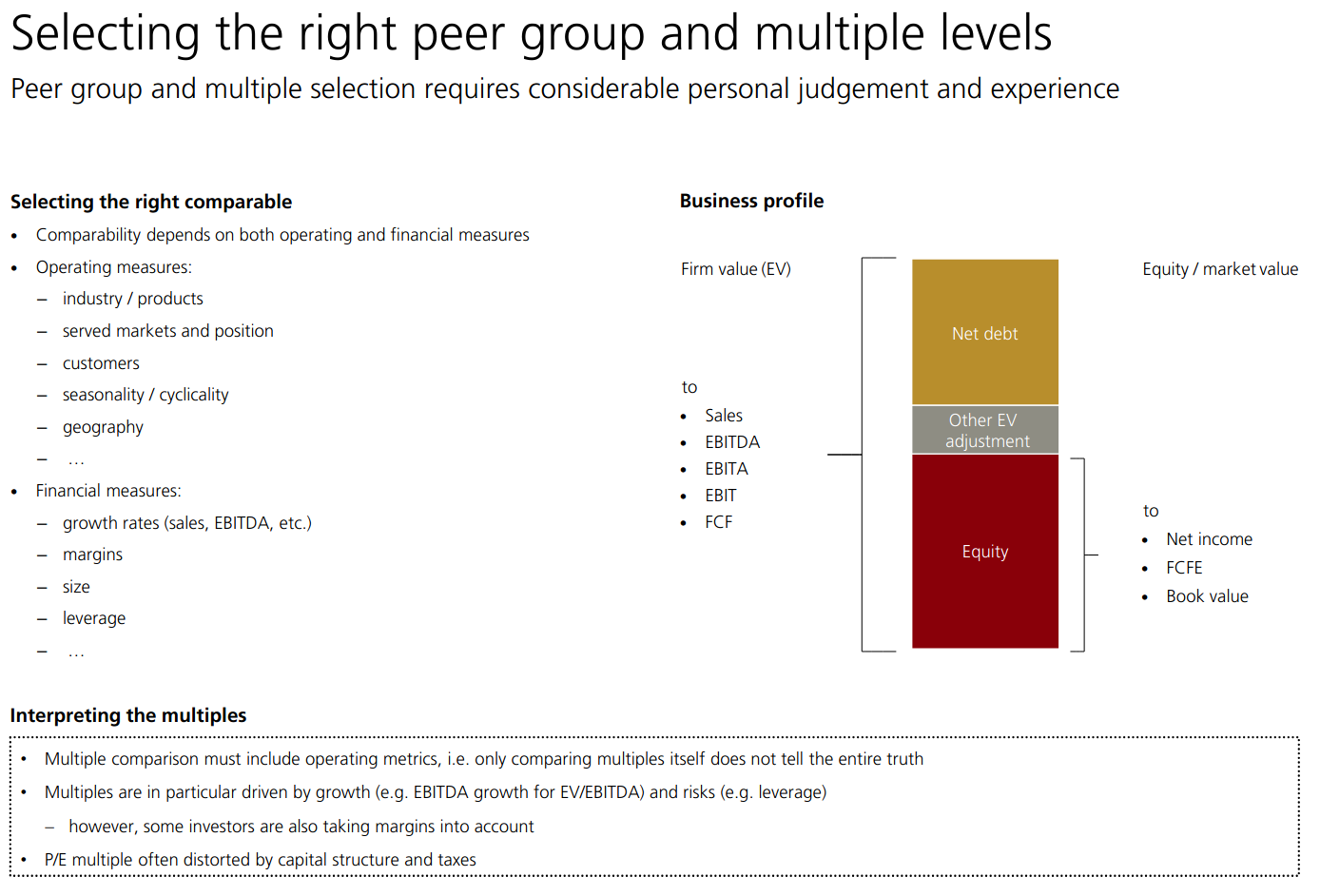

Enterprise Value (EV) vs. Equity Value (EqV)

Interesting: We always use public valuation for Equity Value (not face value of equity) when valuing assets

- but for debts, we don’t use public value but face value!

- weird, because this massively impacts

EqV = share price * diluted shares outstanding (value belonging to equity holders only, i.e. shareholders)

Right side: EV = value of the firm to all stakeholders (debt holders + equity holders)

To calculate EV = EqV + Debt - Cash + Other EV adjustments (so positive for Debts, negative for assets)

- equity investments in associates → decreasees the Other EV adjustments

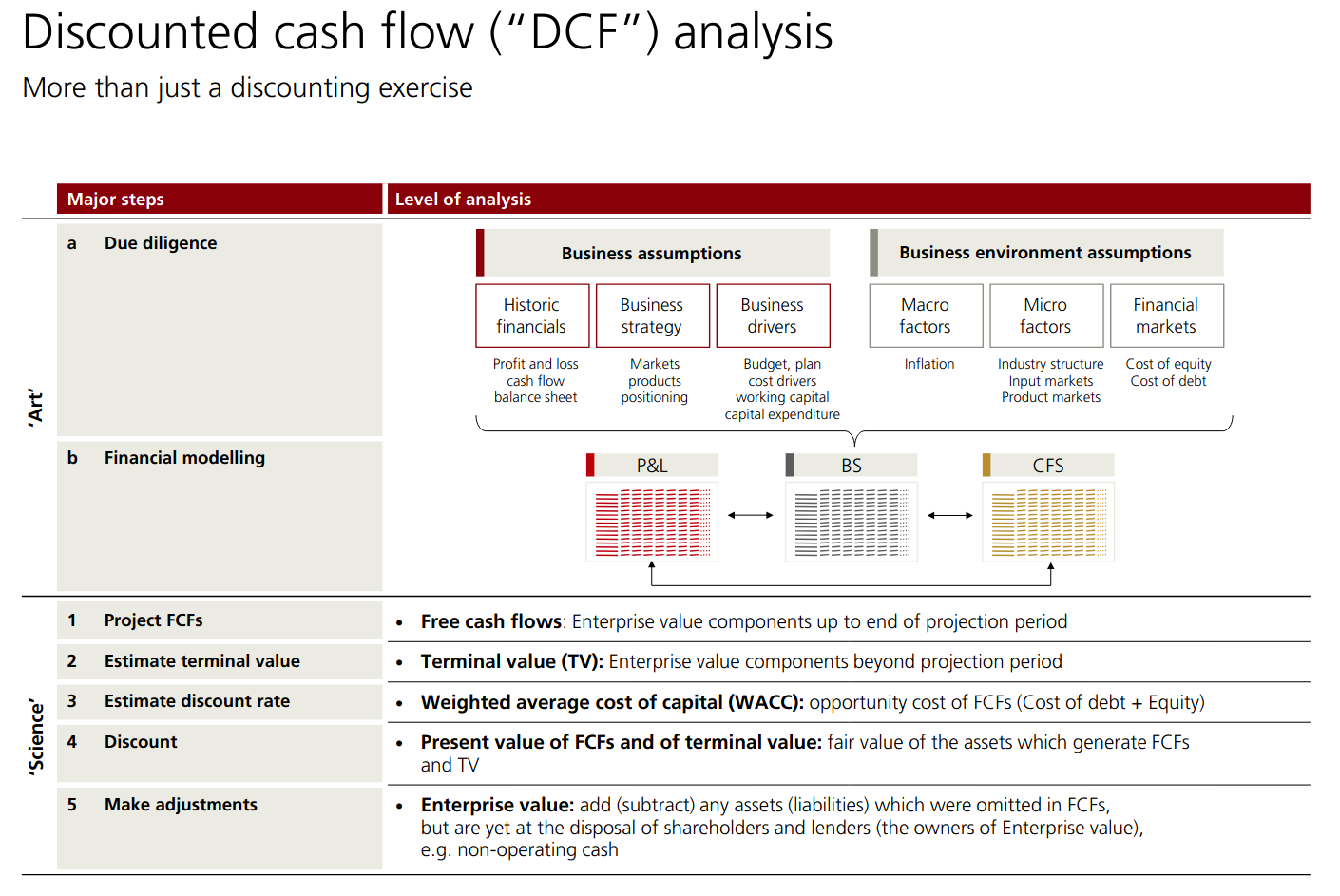

Discounted Cash Flow (DCF) Analysis

There’s a lot of “art” when doing the fundamental assumptions, that influence the hard math models.

UBS always does a DCF

- not for pure dollar values

- play out different scenarios (ukraine spillover into eastern european countries for acquisition with assets in that region for ex)

→ Looking at the volatility of the value rather than number

They look at EV / EBITDA → kind of cashflow.

but this is different for each industry

Negotiation Considerations

bankers try to find the deal that works for both parties → very easy to walk away from a deal

Potential Stakeholders

- shareholders, board of directors, management, employees

- external:

- clients:

- research analysts

- capital markets

- unions

- buyer/seller

- rating agencies

- regulators

- general public

- and for both: press, proxy advisors

- clients:

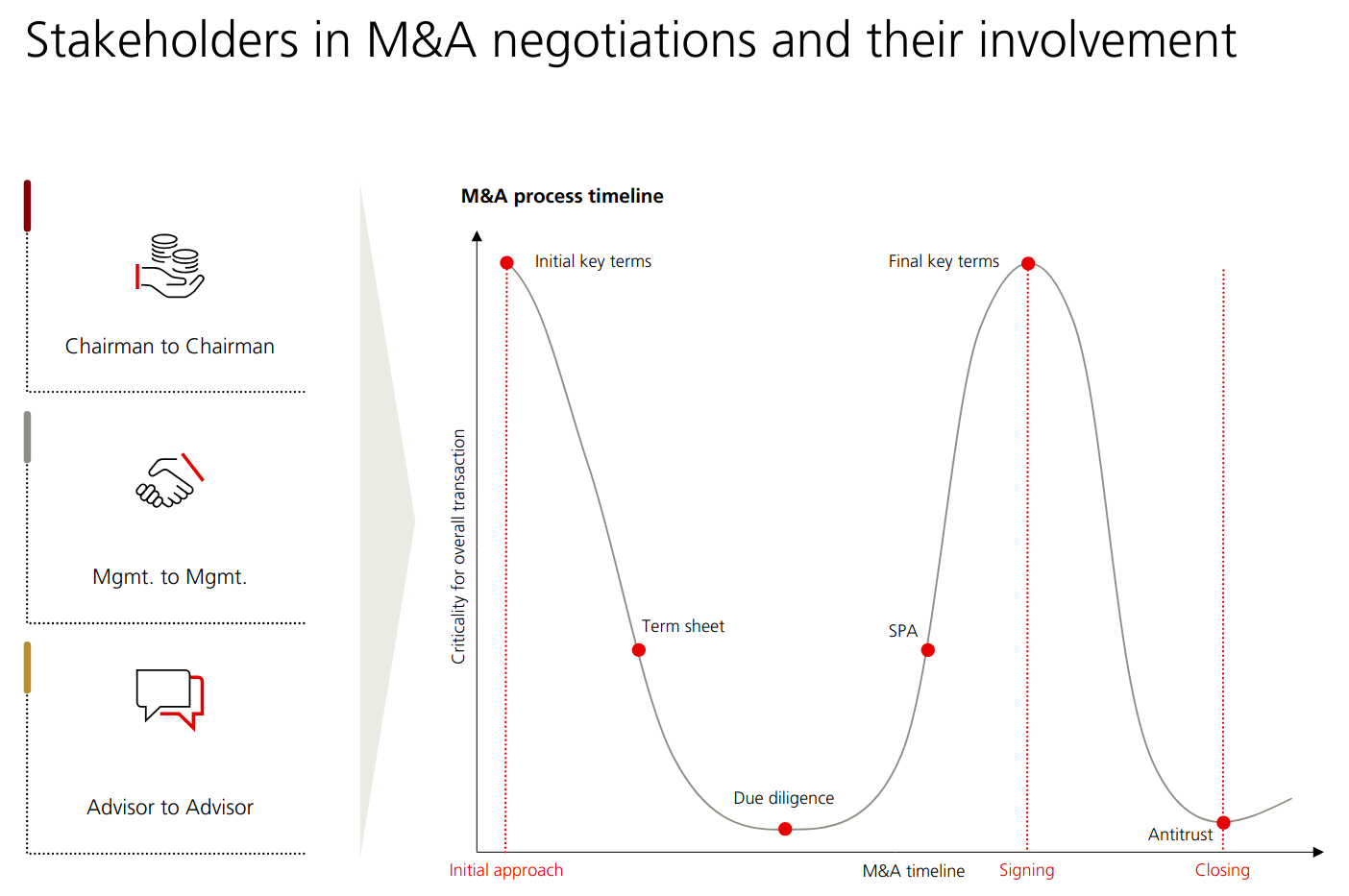

Negotiations are different amongst stakeholders:

- chairman to chairman

- focus on few items → define the transactions

- face to face in person

- mgmt. to mgmt

- more detailed negotiation

- control and oversight function

- advisor to advisor

- negotiate and implement the high-level terms agreed upon by chairmen and management

- support them in tactics and likely outcomes

- → they have experience

They all have a potential hidden agenda

difference in culture

- roche, etc… have entire teams

- some countries different process

Extra

Short

Legal Classifications:

- merger: combines all assets and liabilities into one surviving entity

- stock purchase: buyer acquires stock to control all assets and liabilities

- asset purchase: buyer acquires explicitly determined assets and specific liabilities

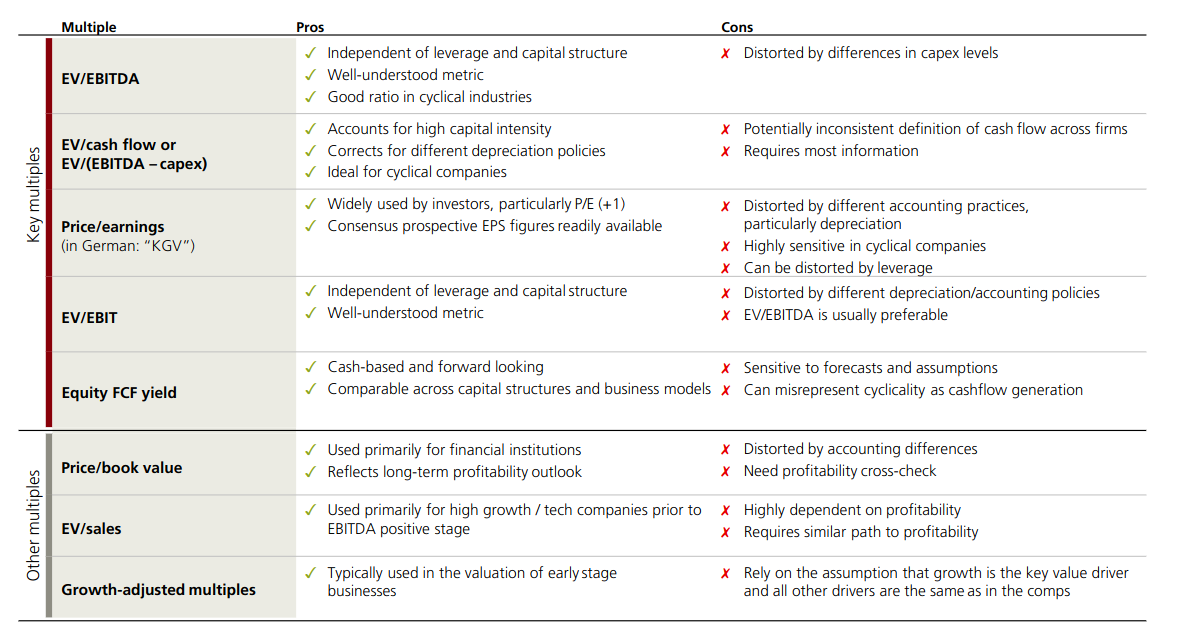

Matching Multiple to Description

-

“Independent of leverage and capital structure; well-understood; good in cyclical industries; BUT distorted by differences in capex levels.” → EV/EBITDA

- capital-structure-neutral, good for cyclicals, but ignores capex differences (hence EV/(EBITDA-capex) for capital-intensive sectors)

-

“Cash-based and forward-looking; comparable across capital structures and business models; but sensitive to forecasts and can misrepresent cyclicality.” → Equity FCF yield

- true cash returns but sensitive to forecasts

-

“Widely used (especially +1); consensus prospective EPS readily available; BUT distorted by accounting practices, depreciation, leverage, and is highly sensitive in cyclical companies.” → P/E

- bottom-line, distorted by depreciation/leverage/taxes

-

“Used primarily for financial institutions; reflects long-term profitability outlook; BUT distorted by accounting differences and requires a profitability cross-check.” → P/B

- primarily for financial institutions

-

“Used primarily for high-growth/tech companies prior to EBITDA-positive stage; highly dependent on profitability and requires similar path to profitability.” → EV/Sales

- for pre-EBITDA growth companies.

Multiples in Short

Cyclicality

EV/EBITDA is better than P/E in cyclical industries, because EV/EBITDA is unaffected by extra leverage taken on during downturns → EV & EBITDA are before taxes

P/E → Earnings collapse at low-turns and surge at the peak, making cycle to cycle and firm/firm comparisons useless.

Familiarity

P/E is widely used and widely compared → familiar to investors

however, it’s also very distorted.

Leverage

- EV/EBITDA is calculated before interest payments, so it sits above the debt line — the multiple is the same regardless of how a firm is financed.

- P/E is computed on net income, which is after interest

- meaning a more leveraged firm reports lower earnings and thus a higher P/E even if the underlying business is identical.

This makes P/E unreliable when comparing firms with different capital structures.

CapEx Levels

EV/EBITDA is influenced by CapEx levels → higher CapEx shrinks EBITDA.

For that we use EV/Cashflow or EV/(EBITDA - capex).

EBITDA ignores capex entirely, so two firms with very different investment needs (e.g. one leasing equipment, one owning it) will look artificially comparable.

Two firms, identical EBITDA of €100m. Firm A spends €10m/year on capex, Firm B spends €60m/year. EV/EBITDA treats them identically. EV/(EBITDA − capex) gives Firm B a much higher multiple for the same EV, correctly reflecting that its “real” cash generation is far lower.

- buy new machine for $ 100m cash

- Cash (asset) - 100m

- PP&E (asset) + 100m

→ Net effect on income is 0 → capex invisible to EBITDA

- Depreciation

- over time, we add the value of the asset

- Depreciation +10m (income statement → reduces EBIT)

- Accumulated Depreciation +10m (balance sheet → reduces PP&E book value)

→ the CapEx spends gets released gradually …

But with EBITDA, we remove depreciation → makes the asset invisible.