if Admin notes:

- what will be asked on the guest lectures

- very conceptual, broad questions → strategic

- “human judgement” not math

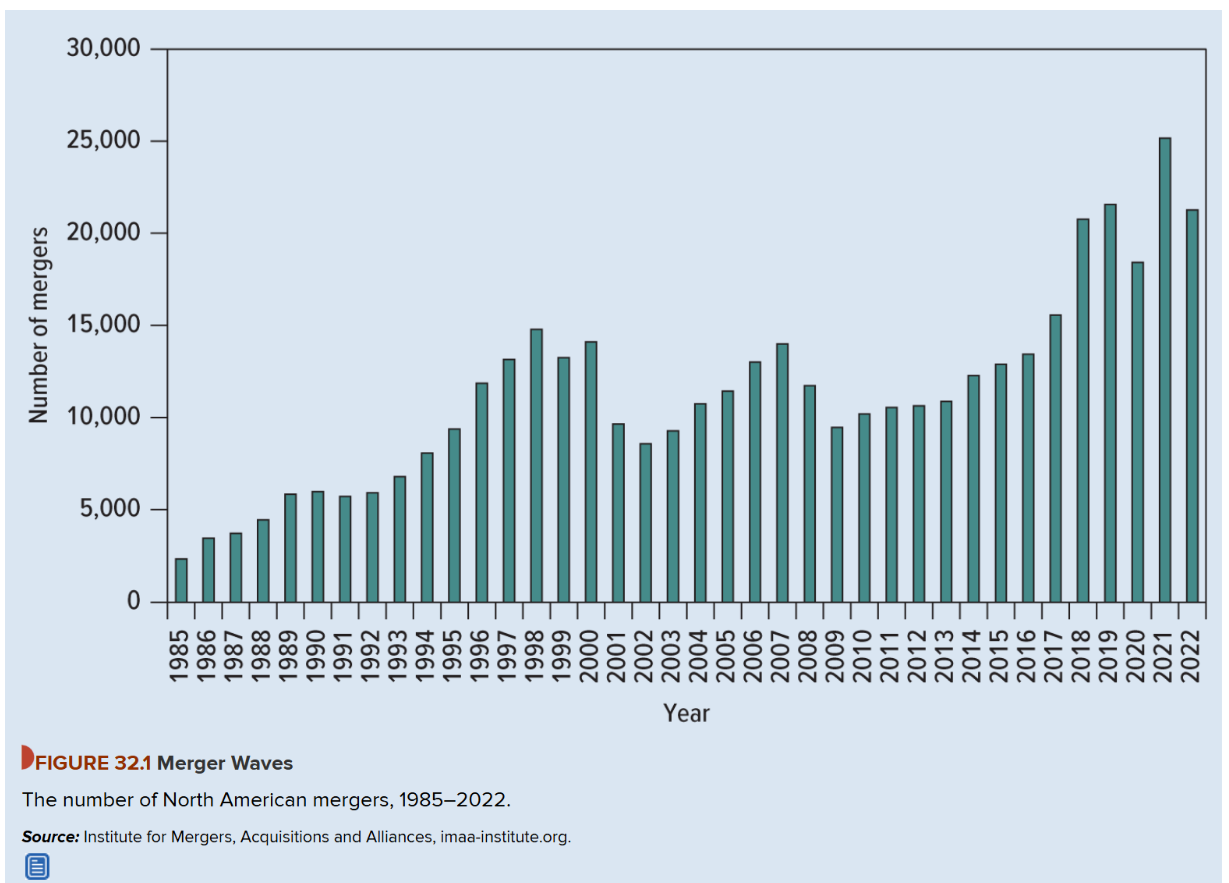

Merger history

Mergers

Types of merger

- Horizontal Merger

- two firms in the same line of business

- Vertical Merger

- companies at different stages of productions

- Conglomerate Merger

- companies in unrelated lines of business

Examples:

- IBM acquires Dell → horizontal

- Walmart acquires Apple production company → vertical

- IBM acquires walmart → conglomerate

Motives for mergers

economies of scale

- larger firm can reduce per-unit costs by using excess capacities or spreading fixed costs more

economies of scope - P&G merger with Merck → P&G marketing economies from selling Merck vitamin and food supplements to P&G existing over-the-counter medicines

- economic advantage to broadening the firms range of products

economies vertical integration - control over suppliers “may” reduce costs

- overintegration can cause the opposite effect

- dubious:

- we buy for 10 from them, but it probably only costs them 6

- the merger cost will include the PV of all future profits already, firm is not stupid

complimentary ressources

- merging may result in each firm filling in “missing pieces” of their firm with other firm pieces

- ex; Roche and some other pharma → one was good at R&D other at launching and promoting

industry consolidation - if industry has many firms competing for same market you get

- excess capacities (factories, workers, sitting idle)

- margin pressure because of undercutting

- inefficient ressource alloc

- M&A is “fix” as it reduces fixed cost by merging firms

- pricing power gain as well, as not that many competing for margins

- shutdown redundant facilities

- Ex: steel in the US → demand dropped after WW2

Tender Offer

Bypasses target firms management → offer directly to shareholders

Qs

- Sellers almost always gain in mergers

- TRUE

- target shareholders almost always receive a premium (20-40%) over the pre-announcement share price

- TRUE

- Buyers usually gain more than sellers

- FALSE

- opposite is true → zero or slighly negative abnormal returns

- FALSE

- Firms that do unusually well tend to be acquisition targets

- FALSE

- firms that underperform are attractive

- their stock price is low

- buy cheap, capture upside (not realised value)

- FALSE

- Merger activity in the US varies dramatically from year to year

- TRUE

- well documented waves → 1980 LBO wave, 1990s tech wave, etc…

- driven by credit conditions, market valuations, regulatory cycles

- TRUE

- On average, mergers produce large economic gains

- FALSE

- evidence is mixed at best

- combined (acquirer + target) abnormal returns around merger announcements are positive but modest

- many mergers destroy value for the acquirer

- usually shareholders and customers, etc… are losers

- FALSE

- Tender offers require the approval of the selling firm’s management

- FALSE

- tender offer goes directly to shareholders

- bypasses the hostile management

- FALSE

- The cost of a merger to the buyer equals the gain realized by the seller

- TRUE

- in context of a cash merger, it’s true by definition

- cost to buyer = cash paid - PV(target, standalone)

- gain to seller = cash paid - PV(target, standalone)

- PV(target, standalone) = present value of the target firm, as if the merger never happened

- what the targets future cashflows are worth on their own.

- usually approximated by Price target shares * # shares = marketcap

- The cost to buyer = takeover premium

- PV(target, standalone) = present value of the target firm, as if the merger never happened

- these are identical

- TRUE

Dubious reasons for mergers

Diversification

- div. is easier and cheaper for the stockholder than for the corporation

- little evidence that investors pay a premium for diversified firm

- ex: ice cream shop buying another firm selling winter goods or something

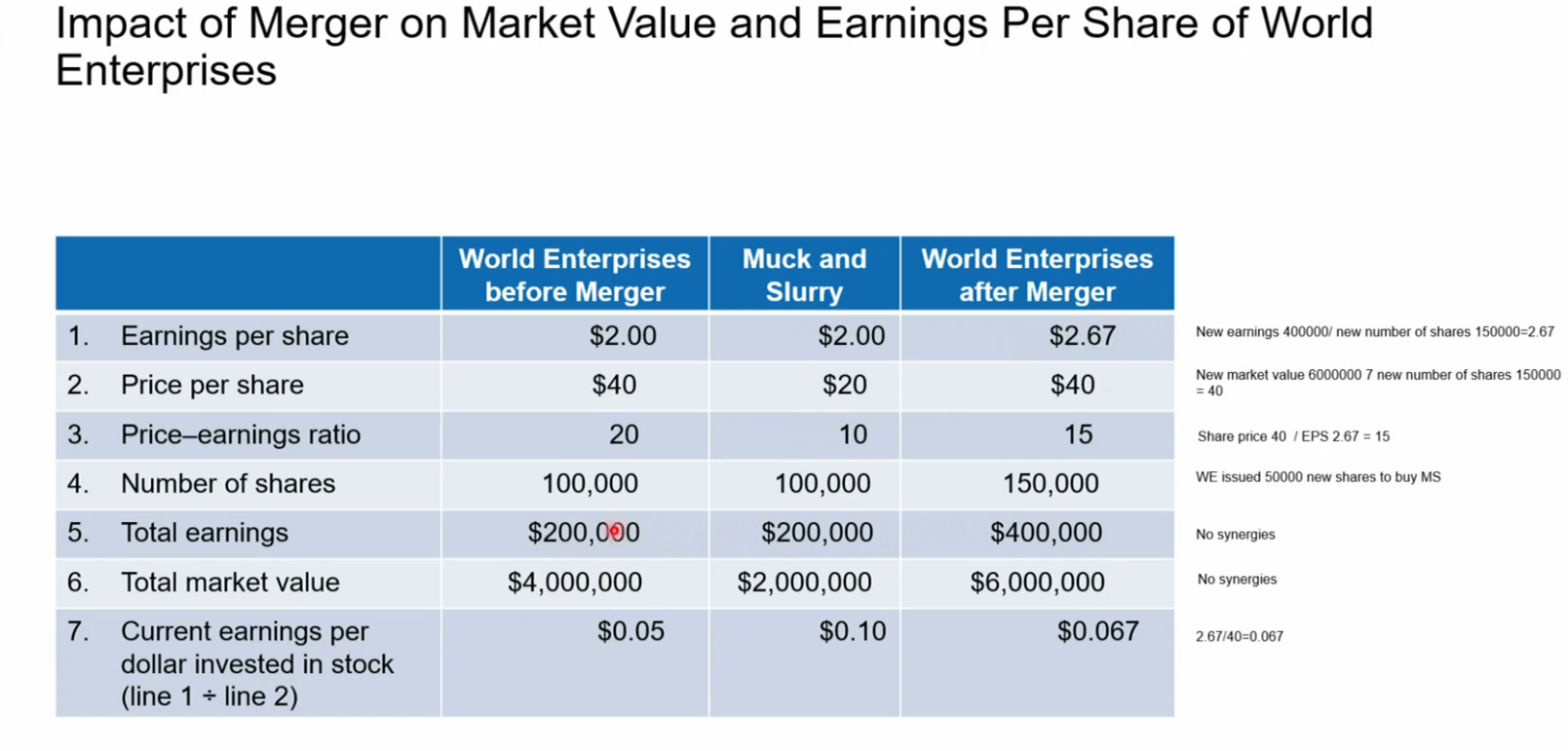

Increasing Earnings per Share bootstrap game - acquiring firm has high P/E ratio

- selling firm has low P/E ratio

- after merger, acquiring firm has short-term EPS price

- long term, acquirer ill have slower than normal EPS growth due to share dilution

Lower borrowing costs - Suppose A, T merge to AT

- As AT’s debts are now backed by the combined assets, the demanded bond yield (i.e. interest rate on their debt) falls → economies of scale?

- No, because the value of the default-put for shareholders decreased (more assets)

- so they lost something → balances out4

Management Motives

- so they lost something → balances out4

- manager hubris

- personal objectives (salary increase, reputation)

- unusual self-esteem → more frequent and larger acquisitions → higher premiums paid, value destroying mergers (empirical evidence)

Defs:

- P/E: price / earnings = market price per share / EPS

- how much investors are willing to pay per dollar of company earnings

- high p/e suggests investors expect future growth

- low p/e suggest undervalued or struggling company

- meaningful only if compared apples to apples

- EPS: earnings per share

- = (net income - preferred divididends) / (weighted avg. shares outstanding)

- net profit divided by number of oustanding shares → how much profit is attributable to each share

Example increasing eps

in this ex: total market value = 4M by A + 400k → 50k new shares issued by A to buy B → total 150k shares

- leads to higher eps

- long term not useful

Estimating Merger Gains and Costs

Not very precise → synergies hard to predict

Merger Gain

The economic gain of a merger is the synergy created — the value of the combined firm above the sum of its parts:

A merger is economically justified iff , i.e. .

Merger Cost (Cash Deal)

In a cash acquisition, the cost to the acquirer is the premium paid above the target’s standalone value:

NPV of a Merger (Acquirer's Perspective)

The NPV to the acquiring firm is:

The merger creates value for the acquirer iff , i.e. the synergy exceeds the premium paid.

Intuitive: Value with merger - value without merger

The gain is the total pie created; the cost is the slice handed to target shareholders via the premium. Even if , overpaying destroys value for the acquirer.

Stock Financing of a Merger

In a stock deal, the cost depends on the post-merger value of the shares given to the target. → If post-merge shares rise more in price, the cost is more

Let be the fraction of the combined firm’s equity given to target shareholders:

Note the key difference from a cash deal: the cost is uncertain ex-ante since it depends on , the post-merger value.

Example: , , , so . Target receives of the combined firm.

Note: if you think that the combined value will actually outperform expectations, rather finance with cash → otherwise acquired firms will get extra free money.

(Their share is worth more than originally thought.)

Thus: if a company prefers a cash deal → the managers of the acquiring firm are optimistic about the post-merger value of their firm.

What if target’s stock price anticipates merger

The Market Value of T might anticipate the merger, and thus rise.

If we pay 65M cash for T, but is actually only worth as the sharerprice already rose by 21M15M$.

Mergers, Antitrust Law, Popular Opposition

Clayton Act

By Clayton Act of 1914 (US) In the US an acquisition is forbidden if “in any line of commerce or any section of the country” the effect “may be substantially to lessen competition or to tend to create a monopoly.

EU Commission: GE’s $46bn takeover bid for honeywell was blocked

Political Pressure:

- national governments being involved in hostile bids

- e.g. 2005 pepsico bid for danone in the EU

- review of acquisitions which have major implications for national interests

- takeover of qualcomm by singapore based broadcom

- → technology USPs → much more detail now (national security)

Forms of acquisitions

One -step (or statutory Merger)

needs the approval of at least 50% of T’s shareholders

Two-step or Takeover

Bid is made to the shareholders to buy T’s stock in exchange for cash, shares or other securities

The second step, after gaining control, is then to vote to complete the merger with the new majority.

Buy all assets

Simply buy the assets of T outright from the firm (directly, instead of the shareholders).

Merger Accounting

How you combine two companies balance sheets

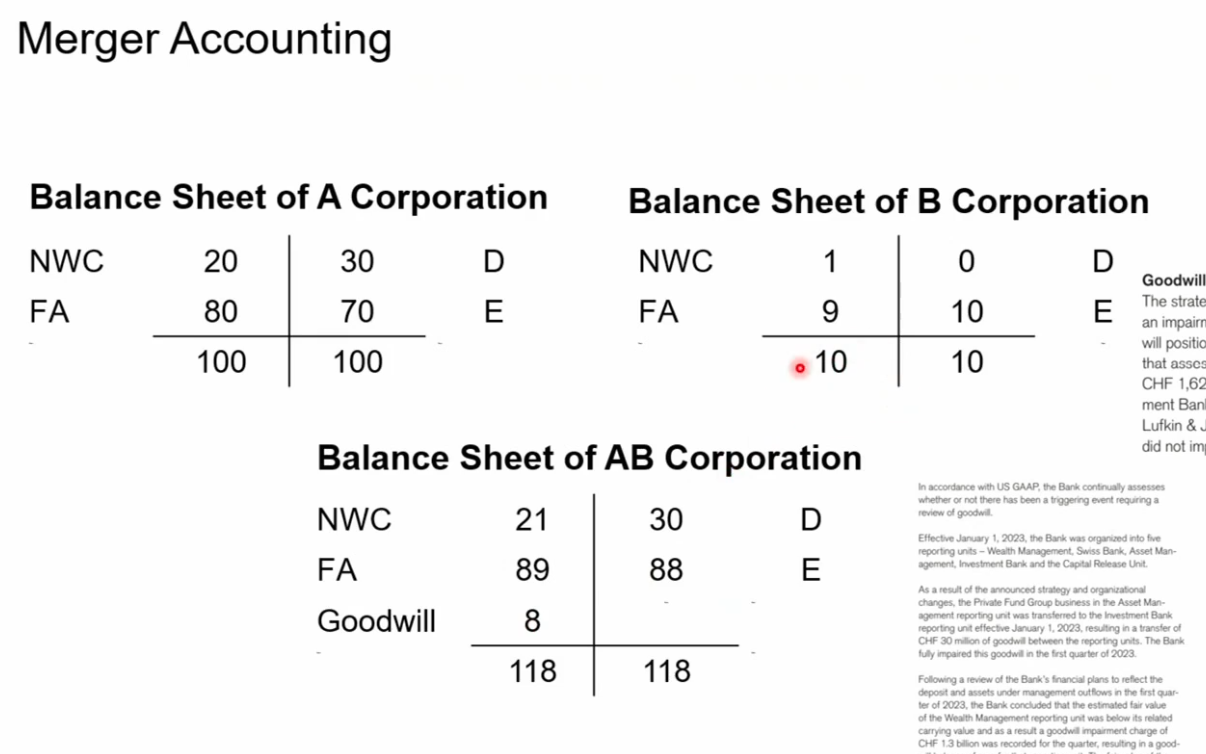

The acquirer records the target’s assets and liabilities at fair value, with any excess purchase price recognised as goodwill.

Goodwill

When company acquires company for a purchase price and has net book value , then

Goodwill is recorded as an intangible asset on the consolidated balance sheet. It captures value not reflected in book figures — brand, synergies, customer relationships, etc.

Example: (book value 100) acquires (book value 10) for a price of 18.

| A | B | AB (consolidated) | |

|---|---|---|---|

| NWC | 20 | 1 | 21 |

| FA | 80 | 9 | 89 |

| Goodwill | — | — | 8 |

| Total Assets | 100 | 10 | 118 |

| Debt | 30 | 0 | 30 |

| Equity | 70 | 10 | 88 |

| Total L+E | 100 | 10 | 118 |

Goodwill . Equity rises by on the acquirer’s consolidated sheet.

Goodwill Impairment

Under IFRS and US GAAP, goodwill is not amortised. Instead it is tested for impairment at least annually. If the carrying value of the reporting unit falls below its estimated fair value, an impairment charge is recognised in the income statement, reducing goodwill on the balance sheet.

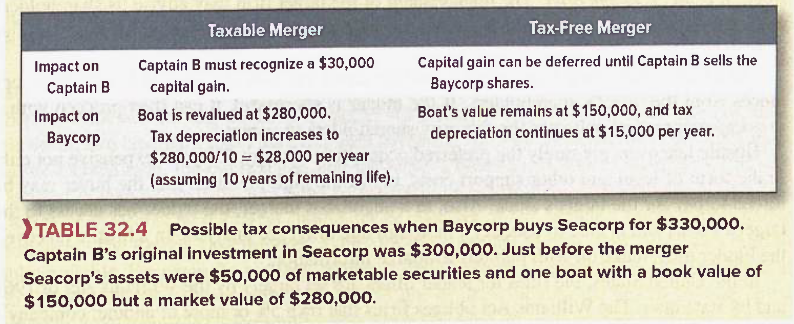

Tax

Tax implications of a merger

- if the shares are bought outright for cash

- → taxable

- if they’re mostly exchanged

- not taxable income

Example, captain B has a boat bought for 300k, depreciates over 20 years, so 15k a year. After 10 years, realises boat is actually worth 280k due to good maintenance.

Takeovers and the Market for Corporate Control

Value of a firm can be increased by changing the management team → market for corporate control = market which takes care of matching up management and firm.

Proxy Contests

- proxy is the right to vote anothers shareholder’s shares

- dissident shareholders attempt to obtain enough proxies to elect their own slate to the Board of directors and try to exchange the management team

Takeovers - tender offer of cash directly to the shareholders

- exchange offer of stock and cash directly to shareholders

- if successful, new owner is free to make any management changes

In the US, if you have more than 5% of other companies stock, you must do SEC filing, stating your intentions

→ often invitation for other bids

If unsuccesfull, at least you can sell your > 5% for a substantial premium

The board also has the duty to carefully evaluate any bid for it’s value → cannot blindly implement defenses without being challenged in court

The managers must obtain the best value possible → cannot reject lower bids from other companies due to golden parachutes / personal interest.

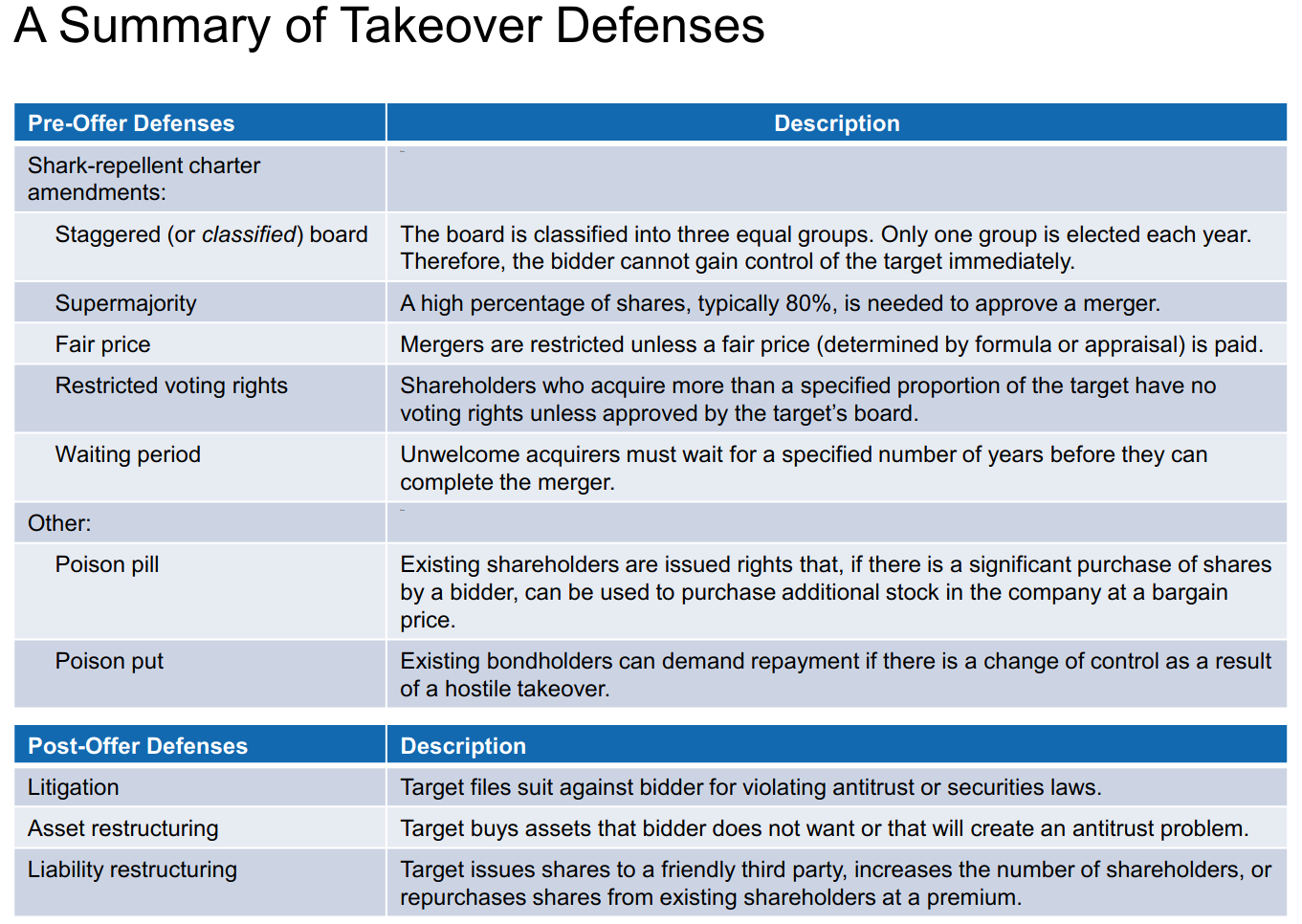

Takeover defenses

defend against hostile takeovers

white knight

- friendly potential acquirer sought by a target company threatened by an unwelcome suitor

shark repellent - amendments to a company charter made to forestall takeover attempts

poison pill - measure taken by a target firm to avoid acquisition

- for ex: right for existing shareholders to buy additional shares at an attractive price if a bidder acquires a large holding

Merger Profitability

Who usually benefits

- shareholders of target (16.1% abnormal return for shareholders → price rises)

- lawyers and brokers

- executives of the acquiring firm

who usually loses

- shareholders of existing firm → overpayment

- executives of the target

- employees due to restructuring

- customers → competition reduced (horizontal)

- bondholders → merger debt is refinanced

- swaps old debt for new debt → usually worse terms, etc…

- bondholders get par/face value, but lose out on created value

- due to callbacks (at call price, not market value which is usually higher)

- credit quality deterioration (maybe due to LBO)

- ex; 4% instead of 6% if interest rates dropped → can’t reinvest at same rates

why acquirer loses?

- usually acquirer much larger → profits due to merger don’t show up in the shareprice

- competition for the company pumps up price artificially (especially with white knights)

- manager hubris

Leverage Buyouts (LBO)

easier with lower interest rates → negative interest rates makes this attractive business

LBO

Large portion of buyout financed by debt (Leverage)

⇒ shares of the LBO no longer trade on the open market

they literally buy out the entire shares → take private

Special case: MBO (management buyout) is buyout lead by existing management.

Leverage: the acquirer (typically a PE firm) puts up a relatively small equity check and finances the bulk of the purchase price with debt, which gets loaded onto the target company’s balance sheet.

- The target’s own cash flows are then used to service and repay that debt over time.

usually after 4-7 years re-IPO or sale to strategic acquirer (or other PE firm)

When interest rates where low → 90% LBOs → now with basel III you need to have % of RWA as capital etc… so this is not possible anymore

RWA → risk-weighted assets (measure used in banking regulation)

LBO loans are RWA-heavy

The debt in an LBO (leveraged loans, high-yield bonds) is extended to a highly leveraged, often unrated or sub-investment-grade company. Under Basel III, these carry 100%+ risk weights — so they consume a lot of bank capital per dollar lent.

- Practical consequences:

- Banks are selective about how much leveraged lending they do, because each loan eats into their capital ratios. If RWA gets too high relative to their CET1 capital, they breach regulatory minimums.

- Syndication: banks rarely hold LBO debt on their own balance sheet. They underwrite the loan and then syndicate it out to institutional investors (CLOs, hedge funds, credit funds) who are not subject to Basel RWA rules. This moves the risk off the bank’s balance sheet and frees up capital.

- Pricing: the RWA cost gets baked into the interest rate the PE firm pays. Higher capital consumption → bank demands higher spread to hit its return hurdle.

→ LBO rates declined after 2022, since the amount of interest expense that can be deducted for tax purposes is not limited to 30% of EBIT.

LBOs in CH:

Ex: CVC acquired sunrise in CH → listed it afterwards

Main Ways LBOs extract (create) Value

- junk bond market → LBOS financed with “junk” debt

- taxes → debt interest is tax-deductible → creates tax shield boosting after tax returns

- other stakeholders

- value can be transferred from employees,suppliers,bondholders to equity holders (cutting wages, renegotiating contracts, etc..)

- high debt forces management discipline → must generate cash to service debt

- equity stakes align management incentives with the owner

- leveraged restructurings

- post-buyout, the firm is restructured (asset sales, cost custs) to unlock hidden value

Leveraged Restructurings

→ difference between LBO and ordinary acquisitions

- large fraction of purchase price is debt financed

- LBO goes private → no longer traded on the market

LBO main characteristics

- high debt

- incentives

- management usually gets equity stakes, aligning their interests with making the company profitable

- private ownership

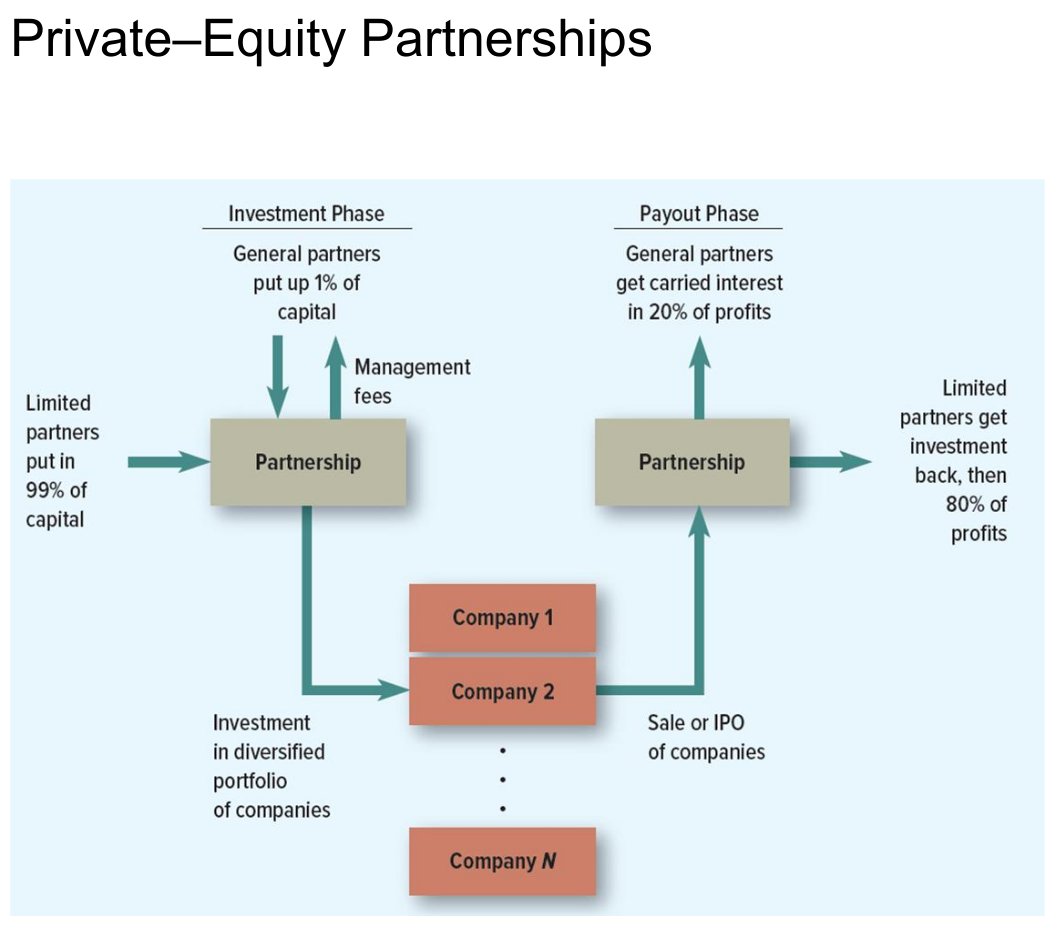

Private-Equity Partnerships

Pe usually very private → not easy to invest in there

Exam Answer: Private-Equity partnerships manage investment funds that buy firms with an eye to improving target-firm value.

GP sets up and manages the partnerships.

LP give most of the money (99%) → no active role

After initial investment is returned LPs get 80% of any profits

GPs get yearly management fee and carried interest 20% on the returns exceeding initial investment.

Limited term, 10 years or less.

Two ways to cash out: At the end of the term, the portfolio is sold (IPO or to another firm).

A private equity (PE) fund operates as a limited partnership between two classes of partners. The fund raises capital, deploys it into a portfolio of private companies, and eventually exits those investments, distributing the proceeds.

Why typically 10 years? Limited partners require it to ensure cash flow is returned, focus is maintained on reorganizing target firms, and risk-taking incentives via carried interest are preserved.

General Partner (GP)

The general partner manages the fund. GPs contribute 1% of the total capital and are responsible for sourcing deals, executing investments, and managing portfolio companies. In return, they collect management fees (typically ~2% of AUM annually) during the investment phase.

Limited Partner (LP)

Limited partners are the passive investors — pension funds, endowments, family offices, sovereign wealth funds, etc. They contribute 99% of the capital but have no role in fund management. Their liability is limited to their invested amount.

Carried Interest

Carried interest (“carry”) is the GP’s share of profits on exit. The standard structure is 20% of profits to the GP, but only after LPs have first received their invested capital back (the hurdle). The remaining 80% of profits go to the LPs.

The life of a PE fund splits into two distinct phases:

-

Investment Phase

- The partnership pools capital and deploys it into a diversified portfolio of private companies (Company , Company , , Company ). The GP actively manages these holdings, funded partly by the management fees it draws from the partnership.

-

Payout Phase

- Portfolio companies are exited via sale (to a strategic buyer or another PE fund) or IPO (initial public offering on a public exchange). The proceeds flow back into the partnership and are distributed as follows:

- LPs receive their original capital back in full.

- Remaining profits are split: 80% to LPs, 20% to the GP (carried interest).

- Portfolio companies are exited via sale (to a strategic buyer or another PE fund) or IPO (initial public offering on a public exchange). The proceeds flow back into the partnership and are distributed as follows:

Profit Sharing Summary

Let be total invested capital (with LPs contributing and the GP ) and let be the total exit value. Define profits . Then:>

The GP’s economic leverage is significant: having put in only 1% of capital, the GP captures 20% of upside.

Example: Suppose a fund raises \1\text{B}$990\text{M}$10\text{M}$2\text{B}\Pi = $1\text{B}$990\text{M} + $800\text{M} = $1.79\text{B}$10\text{M} + $200\text{M} = $210\text{M}21\times$10\text{M}$ stake.

Extra

Chapter 7 vs. Chapter 11 of US Bankruptcy

Chapter 7 oversees the firm’s LIQUIDATION (“death and dismemberment”); Chapter 11 attempts to NURSE the firm back to health through reorganization.

P/E Ratio

Price-to-Earnings Ratio

For a publicly traded company, the price-to-earnings ratio is the price paid per unit of annual earnings:

where is the price per share and is the earnings per share. A value of means investors pay for each unit of current annual earnings.

Spin-Offs

The announcement of a SPIN-OFF is generally followed by abnormally HIGH stock returns, as investors react favourably to improved focus and incentives.

Advantages:

- They widen investor choice by allowing them to invest in just one part of the business.

- They can improve incentives for managers.

- By spinning off businesses with “poor fit,” parent firms can concentrate on their core businesses.

- They relieve investors of the worry that funds will be siphoned off from one business to support unprofitable capital investments in another

Privatisation

The three motives for privatisation are:

- efficiency

- share ownership

- government revenue

Privatized firms generally GROW FASTER, increasing employment. Massive layoffs are NOT a typical consequence.